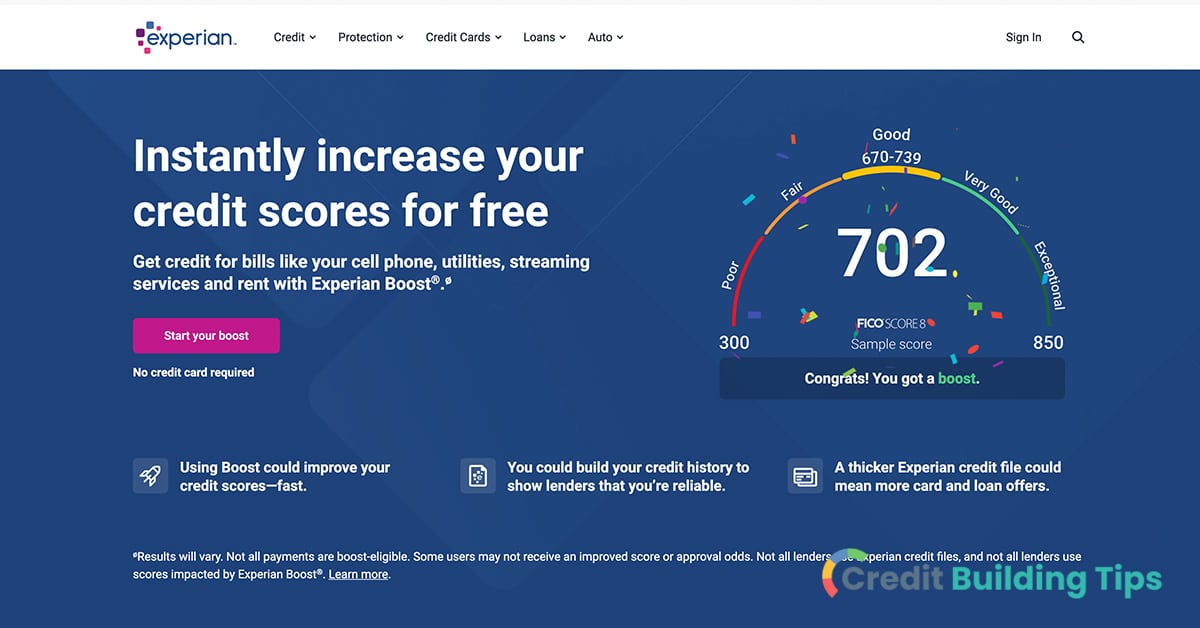

In this post, we'll take a look at how Experian Credit Boost can help build your credit by adding a positive payment history for things like rent, utilities, and subscription streaming services.

The credit system can feel pretty frustrating sometimes-- a person can make regular, on-time payments for a big stack of bills and not receive any recognition for their responsible behavior. Services like Experian Boost can offer a leg up to people with thin credit profiles but years of making bill payments under their belt.

Basically, Experian Boost is a way that you can build your credit history and potentially even instantaneously improve your credit score.

Basically, Experian Boost is a way that you can build your credit history and potentially even instantaneously improve your credit score.Let's take a look at exactly how this service works and whether it's right for you.

Experian Boost is an optional tool you can use to raise your FICO score instantly.

The way this program works is that it allows you to add your positive payment history for things that don't typically show up on your credit report, including rent, utilities, and even subscription streaming services.

Experian Boost is free to use and easy to opt out of if you change your mind. At the same time, you'll have to share your banking and account information with Experian in order to benefit from the service. Before you sign up, it's a good idea to think about whether this is something you feel comfortable with.

According to Experian, the average person that uses Experian Boost will raise their FICO 8 credit score by 13 points.

This credit-building tool can be useful for people who are looking to add a few more points to their credit score and potentially bump them into the next credit bracket.

In addition to helping you increase your credit score instantaneously, Experian Boost offers a number of other free features.

Here are some of the other things you can benefit from when you sign up for this program:

In order to use Experian Boost and gain the benefits of a credit score increase, you have to allow the program to scan your bank account transactions.

By looking at your bank account, Experian Boost will identify rental, cell phone, utility, and streaming payments. They will then include this information in your Experian credit report.

If you're worried that a few missed payments in the past make it so you're not a good candidate for Experian Boost, it's worth noting that they only count positive payment history. This means that missed or late payments for rent, utilities, cell phone service, or streaming services won't hurt your credit score.

The same is not true when it comes to the typical information that shows up on your credit report. If you miss a credit card payment by thirty days or more, for example, a negative mark will show up on your credit report. This will, in most cases, reduce your credit score.

By linking your utility, telecom, and bank accounts to the credit report generated based on your credit history by Experian, you can potentially raise your credit score.

In short, this is letting you get credit for your positive, on-time payments for things like rent, cell service, and utilities. You do have to have at least one active credit account in order to use the service, so it's, unfortunately, not useful to people who are trying to build a credit profile from scratch.

Only certain payments are eligible for Experian Boost, which include:

Your new credit score will be generated instantly once you sign up and link your bills. While it's possible you won't see a change in your credit score after going through this exercise, Experian says that your credit score won't go down when you utilize the service.

Will taking the time to sign up for Experian Boost and link your accounts will result in a higher credit score? The answer is: it depends.

The first important point to make is that using Experian Boost only updates your Experian credit report with your positive payments. This means that if a lender looks at a credit score generated from TransUnion or Equifax, Experian Boost won't be much help.

That being said, Experian says that the most common versions of both the FICO score and VantageScore can be benefited by the service.

Experian Boost is typically most useful for people that don't have a very robust credit history-- i.e., people with a thin credit profile or less than five accounts on their credit report.

The second point is that whether Experian Boost increases your score is going to depend on your particular circumstances.

On the other hand, people who have thin credit profiles might notice a bigger boost when using this program. As a final point, it's important to note that not all payments are eligible for Experian Boost.

The good news about Experian Boost is that, if it does have a positive impact on your score, it will happen in just a few minutes. The sign-up process is relatively simple, and your FICO score will generate quickly after you connect your accounts to your credit file.

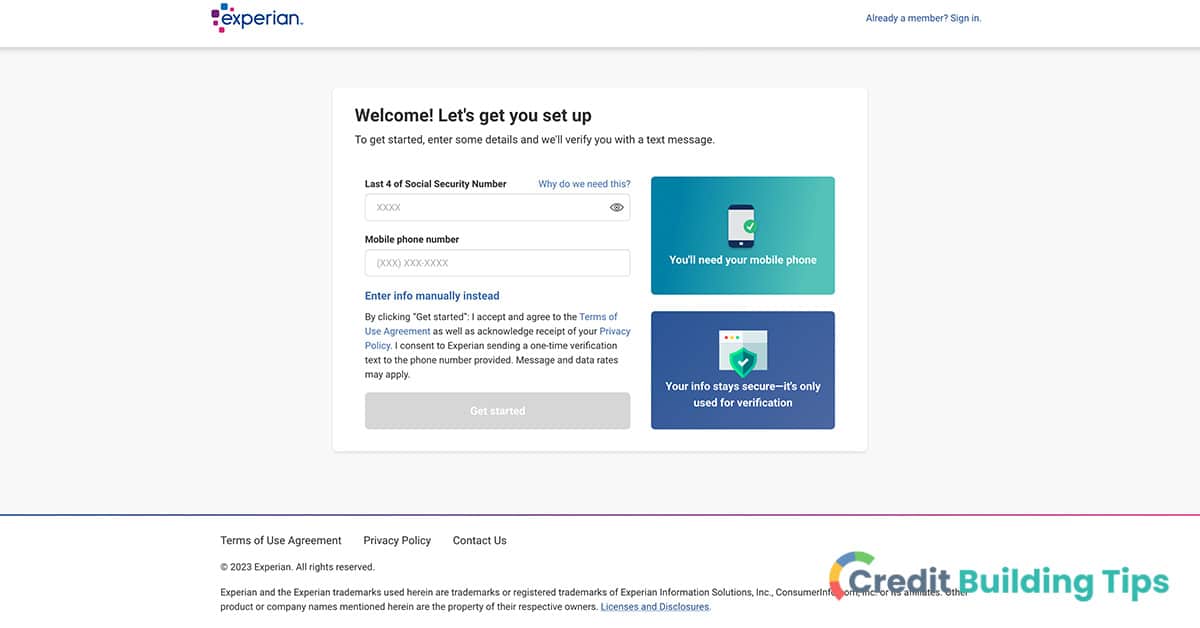

To sign up for Experian Boost, you'll start by going to their sign-up page to create a free Experian account.

From there, you'll follow these steps:

That's it! If you want to take any of your accounts off at a later date, you'll want to sign into your account and navigate to the field titled "Connected Accounts." You can then click "disconnect" for the account you no longer want to show up on your Experian credit file.

Whenever you're signing up for a new service and entering personal information, it's important to understand the pros and cons.

Let's look at some of the things you'll want to know about Experian Boost before you start linking your accounts.

If a lender is using TransUnion or Equifax to generate your credit scores, you're not going to gain any benefit from Experian Boost. For people who are looking to use the service to boost their score before applying for a mortgage or a new credit card, it's important to understand that Experian Boost might not help depending on the credit report a creditor or lender is using.

When you sign up for Experian Boost, you have to link your bank account. This is how they are able to verify that you have made payments on time and add them as tradelines to your credit file.

However, it isn't Experian itself thumbing through your bank statements. They use an intermediary company called Finicity to accomplish this aspect of the process. Before you sign up, it's a good idea to think about whether you feel comfortable letting another company go through your bank account and have access to so much personal information.

If you have excellent credit and a robust credit history, Experian Boost probably isn't worth your time or energy. Even if it does increase your score, five points probably won't offer much in the way of benefits to people with a score of 760 or higher.

Another important thing to consider is that Experian Boost only works with newer versions of the FICO score. Considering that mortgage lenders still generally use older FICO score models, this can mean that it's not worth the effort if your primary purpose is increasing your score before buying a house.

Finally, you'll lose any benefits you gain if you end up opting out of the program. Any extra points you enjoyed will disappear if you aren't actively enrolled.

If you like the idea of Experian Boost but it doesn't quite help you achieve your goals, there are some other options out there. Primarily, you can sign up for another third-party service that helps you boost your score, or you can work to build credit the old-fashioned way.

There are a number of other third-party services on the market that offer similar perks as Experian Boost.

Here are some others you can look into:

Building credit is something anyone can do, but it often takes a bit of time and persistence.

There are a number of things you can do to help increase your scores over time. Here are some crucial steps you can take if you're interested in raising your credit score but don't want to use one of these credit score-boosting services:

Searching for more answers about using Experian Boost? Let's take a look at some of the most frequently asked questions about this credit-building tool.

Experian states that they use bank-level SSL security encryption so that your data is secure and safe. Of course, you are always taking some level of risk when you enter personal and financial information online.

Here are a few tips to ensure you aren't doing more harm than good when using a service like Experian Boost:

If you hand your landlord an envelope of cash on the first of every month, you're not going to be able to benefit from your on-time rent payments through Experian Boost. The same is true if you use a mobile payment transfer app (think Zelle, PayPal, or Venmo), a personal check, or a money order.

In order to have an Experian Boost and benefit from this service, you need to meet the minimum FICO requirements. These are:

If you meet these requirements, then you can use Experian Boost to get your FICO Score.

UltraFICO is another popular service for boosting consumer credit scores, particularly for those who have thin credit files.

This can be useful for people who don't have a FICO score at all or who have a low FICO score. Like Experian Boost, this process works by having you share banking data from your checking, savings, and money market accounts.

By scanning your bank accounts, a number of pieces of information will be collected in order to potentially boost your score, including:

UltraFICO doesn't actually add this information to your credit report. What it does instead is contribute to the calculation of your FICO scores. Since Experian Boost and UltraFICO work in different ways, you can actually use both to help give lenders more information about your creditworthiness.

According to Experian, most people who use their Boost service increase their credit scores instantly.

The people who will benefit the most are those who either:

Only the newer credit scoring models are impacted by the additional information contributed to your report by Experian Boost. This means that the following scoring models can be improved using this service:

If you're looking to add a few points to credit scores generated from your Experian credit report, Experian Boost can be a very useful tool. By letting you add positive payment histories for things like rent, utilities, and streaming services, you might be able to snag a few more points and even get bumped up into the next credit bracket.

At the same time, Experian Boost might not be the right choice for everyone. Those who have robust, long credit histories might not see much benefit from adding their on-time payments using this service. Furthermore, some consumers might not love the idea that they have to give access to their bank accounts to an intermediary service in order to participate.

Whether or not Experian Boost is the right choice for you, taking the time to determine the best way to achieve and maintain a healthy credit score is well worth the effort. Your credit score can have a very real impact on your life, affecting your ability to take out credit lines, buy a house, rent an apartment, and much more.

Are you interested in learning more about how you can improve your credit? Are you searching for more resources to help you become more financially literate? Make sure you check out our Credit Building Tips blog for more useful articles and guides!

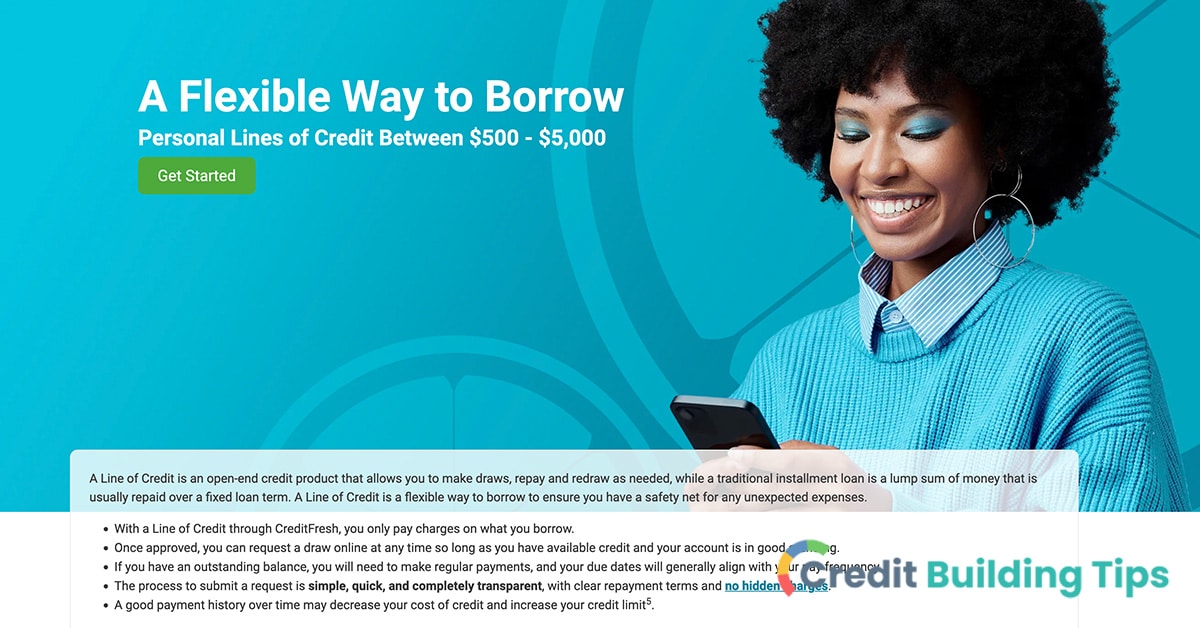

If you need fast access to cash, you might have found a number of online loan and line of credit providers that say you can have money deposited to your account the same day you're approved. One such company is CreditFresh, which advertises that they offer "a flexible way to borrow." So, is Credit Fresh legit, or is it a scam?

The answer to this question depends on what you mean by "scam."

CreditFresh is a legitimate company that offers personal lines of credit to consumers. However, this is a particularly expensive way to borrow money. If you're not careful, you could end up spending a tremendous amount on interest.While it might be useful in a bind when you have no other options, there are generally better, less expensive ways to borrow money. In this article, we'll take a look at everything you need to know about CreditFresh and borrowing money with less-than-ideal credit.

CreditFresh is a company that provides lines of credit through its partnership with a number of financial institutions.

They work with a number of different Bank Lending Partners, including:

When you submit a request for credit using CreditFresh, the line of credit could originate from one of the above-listed banks or another one of their partners.

CreditFresh offers lines of credit to consumers with low credit scores that need to get their hands on some cash fast. While this might seem like a lifesaver if you're in a bind, it's important to understand the costs of borrowing money in this way.

CreditFresh markets the line of credit they offer as straightforward and transparent. It's important to understand the potential costs of borrowing money in this way versus other options.

Any time you're borrowing money, there are a lot of important questions to ask. One key question is: what's the true cost?

In the fine print on CreditFresh's own website, they go so far as to state that borrowing from them is an incredibly costly way to gain access to some cash:

"A Line of Credit through CreditFresh is an expensive form of credit and should not be used as a long-term financial solution."

Though it's difficult to find information on CreditFresh's site about their interest rates, other sources state that the APR for a line of credit starts at 65%.

For the purposes of comparison, the average credit card interest rate as of September 2023 is 24.45%, which is historically quite high, according to Lending Tree.

Already, this should send up some red flags. 65% is an incredibly high interest rate, and that's just where rates start. According to one source, the interest rates are typically under 200% for a line of credit from CreditFresh, which is a recipe for spending an outrageous amount of money during the repayment of the loan.

Is CreditFresh just a scam? Or is it a legitimate company?

CreditFresh is, in fact, a legitimate company that offers lines of credit to consumers through its partnership with various financial institutions.

Don't stop reading just yet, though. Just because CreditFresh isn't a complete scam doesn't mean taking out a line of credit from them is a good idea.

By targeting consumers with low credit scores who need access to cash fast, CreditFresh is taking on a lot of risk. The way that they justify this amount of risk is by charging incredibly high-interest rates for these credit lines.

A little later in the article, we'll talk about the pros and cons of taking out this type of line of credit as well as some alternative options on the table.

First, we'll take a closer look at a recent class action lawsuit that was proposed against CreditFresh regarding concerns surrounding a data breach that occurred in the spring of 2022. Even if the company is technically "legit," the type of activity outlined in the complaint might leave you to think twice about taking out a line of credit from this company.

Another important piece of information you'll want to consider when you're thinking about working with CreditFresh is that a class action lawsuit was proposed against them not long ago due to a data breach.

The proposed class action lawsuit claims that the company didn't protect the personal information of consumers adequately from access by unauthorized parties. The defendant in the proposed suit is Propel Holdings, Inc., which uses the CreditFresh name to offer lines of credit through First Electronic Bank, CBW Bank, and other partners.

The data breach is said to have occurred in February or March 2022. Allegedly, the following information was exposed to both customers and prospective customers:

The lawsuit claims that CreditFresh could have taken reasonable steps to prevent the breach. Consumers who had their information exposed now "face years of constant surveillance of their financial and personal records, monitoring, and loss of rights," according to the complaint.

If you need quick access to cash, it's easy to start making compromises. You might tell yourself that borrowing money at an exorbitant interest rate isn't a big deal because you'll pay it back quickly, or maybe you don't even think about the interest rate because you're in such a desperate financial situation.

The truth is, though, it's ultimately best to steer clear of this type of borrowing option. There are other more affordable alternatives that could help you get the money you need now without threatening your future financial stability. This is true even if you have bad credit-- you just might need to shop around or get creative.

There are lots of online loan providers these days, some of whom will consider borrowers with poor credit scores. You might be able to increase the likelihood that you'll be approved by offering additional information, such as any outstanding debts you have and your employment status.

Another way to gain access to money with a bad credit score is to consider adding a co-applicant who has a stronger credit history.

A secured loan is a way to borrow money for a lower interest rate by putting up an asset as collateral. These types of loans often have less strict credit requirements, but you run the risk of losing the asset if you miss too many payments.

A vehicle can often be used as collateral through online lenders. However, if you apply for a secured loan through a credit union or bank, the collateral usually needs to be an investment or savings account.

Though it can be frustrating and embarrassing to ask your loved ones for a loan, it's possible that this will ultimately be the more financially wise choice if your only other option is a high APR line of credit.

It's important to understand how money can quickly complicate relationships with people, no matter how close you are. For this reason, it's important to hammer out the details of the loan on paper in the form of a contract. Make sure you record how much money you're borrowing, any terms of repayment, and the process through which you'll pay them back.

Lots of credit unions will offer personal loans in small amounts. These loans typically start around $500. When you're working with a local credit union, there's often more leeway in terms of qualification than when you're trying to get a loan from a large, national financial institution.

For example, they might take other information into consideration beyond your credit score, such as your history with the credit union as a member. Personal loan rates are also capped at 18% under federal credit union cap rates.

Are you trying to get access to a line of credit quickly because your bills are getting to be too much to handle? It's possible that setting up payment plans instead of borrowing money could offer the relief you need.

A number of utility companies and creditors will give you the option to fill out hardship forms in order to request an extension. At the end of the day, these entities just want to collect the money they're owed, and they are often more willing to work with you than you might initially expect.

Another option is applying for a loan with a nonprofit lender. There are some organizations, such as the Capital Good Fund, that accept borrowers who have no credit history or thin credit profiles. This particular nonprofit offers emergency loans up to $1,500 and doesn't have a minimum credit score requirement.

The rates for this type of loan can be much more favorable than with for-profit lenders like CreditFresh. For example, the Capital Good Fund offers rates between 5% and 16%.

Payday alternative loans are small loans that some federal credit unions offer. With longer repayment periods and much more reasonable rates than typical payday loans, this type of loan is much less likely to trap you in a cycle of debt.

The National Credit Union Administration created this type of loan program back in 2010. You don't necessarily have to have good credit in order to get a payday alternative loan-- the more important factors include your ability to repay the loan and your income.

If you just need a little extra money to cover your costs until your next paycheck, another option is a cash advance app.

There are a number of popular apps of this type, including:

These apps can be really useful when you're in a pinch, but the truth is they are also a very expensive way to borrow money. Though the associated fees-- whether fast-funding fees or subscription fees-- are very high when weighed against the amount of money you can receive in this manner.

For this reason, cash advance apps are best used in true emergency situations.

At the end of the day, it costs money to borrow money. If you keep finding yourself in a situation where you don't have enough cash to pay for the things you need, you might consider figuring out a way to earn some extra income.

There are lots of ways you can get your hands on cash quickly if you're willing to be a little creative. You probably have some stuff you don't use anymore that could be sold on Craigslist, Facebook Marketplace, or eBay, or maybe you could start a side gig as a rideshare driver. Whether you start hanging signs in your neighborhood offering lawn mowing services or pick up some extra cash babysitting for the neighbor, you don't have to be limited to the income you earn from your day job.

Before I sign off, let's take a look at some commonly asked questions about CreditFresh and other ways to borrow money fast when you don't have great credit.

CreditFresh has been a company since 2019 and provides lines of credit to consumers in roughly half of the states in the U.S. This is a company that specializes in providing fast funding to people with low credit scores. While this might seem like a great deal when you're in a bind, the business model ultimately relies on charging extremely high interest rates in order to justify the risk of lending to consumers who aren't considered particularly creditworthy.

If you apply for a line of credit through CreditFresh and you're approved, your credit limit will range somewhere between $500 and $5000.

There are a number of different factors that are considered to determine your credit limit. You can potentially become eligible for increased credit limits or reduced billing cycle charges based on your payment history.

One of the main selling points of a line of credit through CreditFresh is how quickly the funds can become available to you.

You will typically receive the funds the same day if you are approved and request a draw before 3:30 pm Eastern time during the business week.

If you're approved and request a draw at another time, the funds will show up the next business day.

It's important to remember that your own bank and bank's policies can impact when funds are made available to you.

CreditFresh markets itself as a company that provides clear and transparent disclosures about the cost of borrowing. At the same time, they don't make it clear what interest rates they charge-- other sources state that the APR starts at 65% (which is incredibly high.)

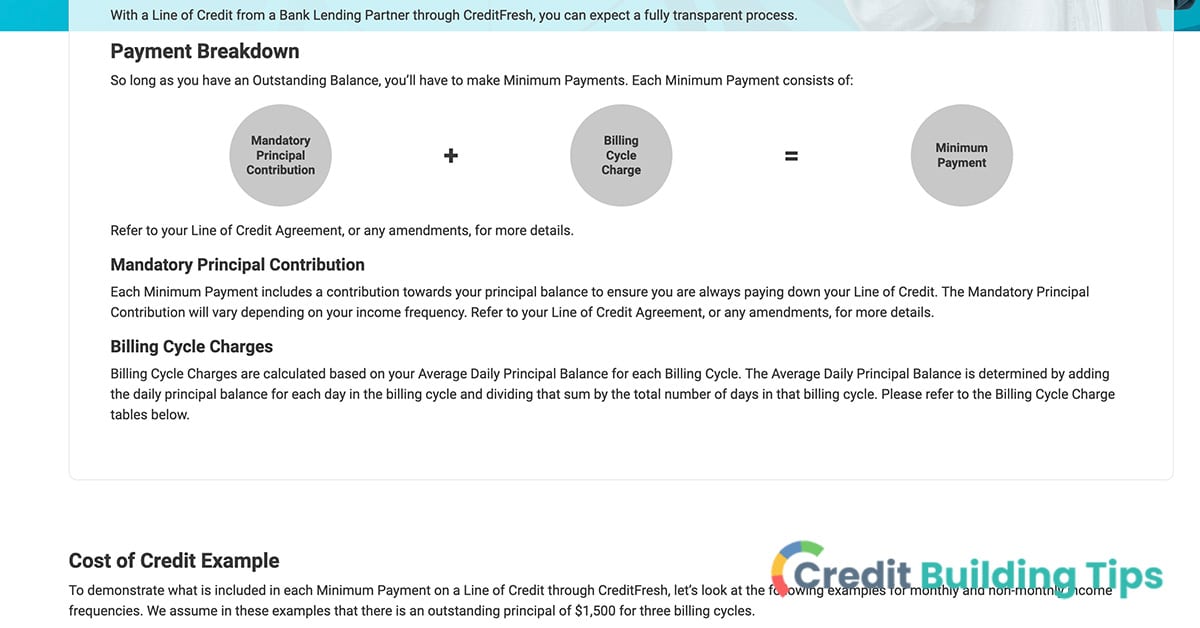

If you have an outstanding principal balance with CreditFresh, you'll have to pay both the billing cycle charges and a mandatory principal contribution as a part of your minimum payment.

When you take out an installment loan or another type of personal loan, you receive a lump sum of money. You then begin repaying the loan over a period of time with additional interest and, potentially, fees. These payments are made in a scheduled manner, typically monthly.

Taking out a line of credit, on the other hand, offers you a credit limit which you can borrow against. This is a revolving line of credit rather than a lump sum loan, meaning that borrowers can draw on their credit line, repay what they owe, and continue to redraw, assuming they have credit available.

There are a few requirements you'll have to meet in order to request a line of credit through CreditFresh.

In order to apply, you must:

As you can see, the bar is pretty low in terms of being able to request a line of credit. There is no minimum credit score disclosed by CreditFresh, but given the nature of the financial product, it is clear they are marketing to people with poor credit scores.

No, you can get a CreditFresh line of credit if you live in certain U.S. states.

These are:

When you have a CreditFresh line of credit, your account status will be reported to TransUnion. TransUnion is one of the three major credit reporting bureaus in the United States. The information that is reported by CreditFresh to TransUnion can be incorporated into your credit score calculation and impact your credit score.

While CreditFresh is a legitimate company, that doesn't necessarily mean opening a line of credit with them is going to be the best financial decision. Offering lines of credit to people with bad credit and charging exorbitant interest in order to deal with the risk, borrowing money from a company like this is quite expensive compared to other potential options on the table.

While there are a few things you can do to quickly boost your credit score, the truth is that it can take a while to improve an imperfect credit file. If you think you might need to take out a loan or get a new credit card down the road, it's a good idea to start thinking about cleaning up your credit report sooner rather than later.

Are you looking for resources to help you out as you work to improve your credit score? Make sure you check out our Credit Building Tips blog for more articles and guides.

Paying off your credit card can feel like a big weight off your shoulders. How long does it take for your payment to reflect in your available balance, though? Will you be able to use your credit card the same day you make a payment?

The answer is it depends.

If you had available credit before your payment, there's no problem using your card on the same day you pay it off so long as you don't exceed your available credit. If your card was maxed out, it could take several days for the payment to process and for the credit to become available to you.If your credit card and your bank account are from the same financial institution, it's possible that your available credit will be updated instantaneously. When money has to be transferred between banks, though, the process typically takes a few business days.

If you've used almost all of your credit limit and you just made a payment toward your card, you might be wondering how quickly you'll be able to use your card for a transaction.

The answer to this question is going to depend on a number of different factors.

The first thing you'll want to know about is the Truth in Lending Act and how it dictates the way that card payments work. According to this Act, credit card issuers have to send you your statement at least 21 days before your payment due date. Furthermore, they must set a cutoff time when they need to receive your payment-- 5 p.m. or later. It's worth noting that if you plan on paying your credit card bill in person at a branch of the financial institution and that branch closes earlier than the cutoff time, the payment will only be considered on time if you pay before the branch closes.

If you paid your bill in a timely manner, you should probably see that your payment is credited on the same business day. If you didn't make the payment before the stated cutoff time, it will likely appear the next business day. At the same time, the fact that the payment is credited doesn't necessarily mean that your balance will be updated. Usually, the payment needs to be processed before it is reflected in your balance.

When you go to make your credit card payment, it's easy to think that the funds should show up immediately once you click "pay."

Sometimes, though, your available credit limit won't change right away. On top of that, it might not show that the funds have been debited from your checking account immediately.

The fact that there's a time delay during the card payment process can be pretty stressful and frustrating. For example, you might be worried that your payment hasn't gone through and that you'll be subject to late fees. Beyond that, you might be waiting to free up some available credit so you can use your card for a purchase.

The truth is, that your credit card payment will likely process practically instantaneously if the bank account and credit card account are through the same bank. However, if you're paying between institutions, there's going to be a bit of lag between the two.

When you're dealing with two different institutions, you can typically expect the transaction to be completed up to three business days after you've made an online payment. If you sent your payment through the mail, it will probably take longer than that.

How many days it will take for your available credit to be updated after payment depends on a number of factors. In most cases, though, you can expect that the credit will be available in one to three business days.

The answer is: that it depends.

If you have maxed out your credit card and are making a payment on the due date, you might have to wait a few days before you have more available credit.

However, if you still have available credit before you make your payment, there is no issue at all with using your card. The transactions you make will end up as a part of the next billing cycle, not as a part of the billing cycle you're currently paying a bill for.

In order for your credit card payment to be considered on time, it simply needs to be submitted by the due date. This means that it doesn't have to be fully processed by the due date-- you simply have to send the payment through.

Once your card issuer acknowledges that you've made the payment, your payment will be credited. Your payment should typically be credited the same business day if you make your payment by a certain time on a business day-- often 5 p.m.

For payments made after this cutoff time or on a non-business day will usually be credited the next business day.

For your credit card payment to fully process, it might take up to three days. However, your payment typically only needs to be submitted by the due date in order to be on time.

What exactly is the difference between a payment being credited and processed?

When you pay off your credit card, it's natural to expect that you should be able to start using it again right away. It can be disconcerting to say the least, to see that there isn't any credit available after you've initiated a large payment.

There are a number of different reasons this could occur. If you have only recently made the payment, the most likely reason is that the payment hasn't finished processing. It may take a few business days for your available credit to reflect the payment that you made.

It's also possible that the credit card issuer has put a hold on your account, which can happen for a number of different reasons. For example, a company might put a hold on the account if:

Delays in available credit can also occur if:

If it seems like there is no good reason for your available credit to still be zero after making a payment, contact your card issuer and ask for an explanation. They will likely be able to get you more information about why this is happening or let you know what steps to take if it does appear to be a mistake of some sort.

It's totally reasonable to want your payment to post quickly. On the one hand, you might want to make sure that there is enough money in your bank account to cover the cost and are therefore interested in the payment occurring sooner rather than later. On the other hand, you might be hoping to free up some available credit so you can continue to use your card.

However, there are a few things you can do to try and make the process go as fast as possible.

Before I sign off, let's take a look at some of the most common questions I receive about making credit card payments.

The best time to pay your credit card bill depends on your circumstances, your financial situation, and your goals.

For instance, if you don't usually use more than 30% of your credit limit and you always pay off the balance in full every month, the timing isn't particularly important so long as you make your payment by the due date.

One of the reasons why it can be beneficial to pay early is that credit card issuers will report to credit bureaus on different dates-- typically around the time of your statement closing date. If you want to make sure your credit score is as healthy as possible, paying before the reporting date can help ensure your credit utilization ratio is on the lower end.

Your credit utilization ratio is one of the main factors in your credit score. The lower your credit utilization, the better. This is a metric that compares the amount of credit available to you to the balance you are currently carrying.

If you want to avoid paying any interest on your credit account, you'll want to pay your bill in full every month on or before the due date.

It's worth noting that you lose your grace period on new purchases if you are carrying a balance from month to month. This is true even for small balances. What this means is that all of your transactions will start accruing interest immediately until the full balance has been paid off.

It's no secret that it's important to pay your credit card bill on time. However, some people say that it's worth going the extra mile and making your payment early. Is this really worth it, and, if so, what are the benefits?

There are a few reasons you might make your credit card payment early.

Whether it's better to pay your bill early or on the due date really has to do with your own financial situation and goals. The most important thing is to make sure the bill is paid by the due date. Otherwise, it can seriously damage your credit score while also leaving you paying a late fee and interest.

Whenever possible, it's a good idea to pay off your credit card balance in full.

When you have a credit card balance carried over from month to month, it can:

Of course, it isn't always possible to pay off your credit card in full every month. In general, though, it's best to put as much money towards it as you can every month. Any amount you can put toward the bill will help to reduce how much-compounded interest you are saddled with.

When you have a large amount of credit card debt you're trying to get a handle on, it's a good idea to trim your discretionary spending and create a strict budget. This will help you find extra money to put towards your bill every month, allowing you to get out of debt faster and reduce the total cost of borrowing.

It's worth noting that there are other ways to borrow money that can be much less expensive than credit cards, such as a personal loan.

If you've been dealing with credit card debt and you've finally paid it off, you might be wondering whether you should just take a pair of scissors to that small plastic rectangle. The truth is, it's generally a good idea to keep your cards open after you've paid your debt unless they have a large annual fee. The reason for this is that closing your account could mean that your credit score goes down, as it can raise your credit utilization ratio.

Ultimately, one of the best things you can do once you've paid off your credit card debt is to start using the money you've been putting toward your card bill and building an emergency fund. According to a study from the Federal Reserve, 40% of Americans would struggle to find the money to pay for a $400 emergency expense. That's a pretty scary place to be, and building an emergency fund can help ensure you don't get caught in a financial pickle.

It's generally recommended that your emergency fund consists of at least three to six months of living expenses. Anything is better than nothing, though, and you might find it's a good goal to save $500 for an emergency fund to begin with.

Whether or not you can use your credit card on the same day you make a payment is going to depend. If you have plenty of available credit before you make your payment, using it on the same day won't be a problem at all so long as you don't try to spend more than what is available to you.

On the other hand, if your card is maxed out and you just made a payment, you might not be able to use it the same day. How quickly credit is made available to you depends on your bank and your credit card issuer. If your credit card and bank account are from the same financial institution, the payment might be processed instantaneously, and the credit will be made available right away.

Are you working to build a greater understanding of credit and credit cards to ensure you have as many financial opportunities as possible down the road? If so, you're in the right place!

Make sure you check out the rest of our Credit Building Tips blog for more resources, guides, and articles to help you improve your credit.

When a portion of your wages is being directly taken out of your paycheck to repay a debt, it's known as wage garnishment. Considering that this process can take a seriously negative toll on your finances, you probably have a lot of unanswered questions. One of the most common things people ask me about wage garnishment is "How long can a creditor garnish my wages?"

While statutes of limitations found under state law often limit how much time a creditor has to take legal action against you for an unpaid debt, these don't apply to how long wage garnishment can continue for.

Wage garnishment will typically continue until the debt has been repaid. This means it can go on for ten years or even longer, depending on the amount you owe and how long it takes you to pay it in full.At the same time, there are some options on the table if wage garnishment is causing you serious financial hardship. Your choices will depend on the type of debt and a number of other factors.

Yes, a creditor can garnish your wages in some instances. For some types of debts, including child support and alimony, unpaid income taxes, and federal student loan debts, a court order is not necessary for money to start being taken from your paycheck.

For most other types of debt, though, the creditor will need to:

There are a number of different types of debts that could result in wage garnishment through a court order.

Some examples of debts that creditors can pursue in this way include:

In order to begin garnishing wages, creditors typically have to sue you and receive a money judgment and court order in their favor. Creditors won't be able to immediately garnish your wages for most types of debt, such as medical bills and credit card bills.

That being said, some creditors don't have to go to court before they start taking money from your paycheck. There are special rules for three types of debt because they are viewed as important enough to ensure the debt can be collected.

These types of debt are:

There is automatically a wage withholding order included in child support orders. Your wages can, therefore, be garnished when you're ordered to pay child support without the court needing to take any additional action. If you fail to pay either child support or alimony obligations, a wage garnishment order against you can also be obtained.

It's worth noting that the wage garnishment limits for alimony and child support are significantly higher than for things like credit card debt or unpaid bills. The limits for wage garnishment for child support under federal law are:

If you've fallen behind on your payments by twelve weeks or more, the cap on your garnishment can be increased by another five percent.

The federal government can also start garnishing your wages without needing to get a court order if you owe back taxes. Your deduction amounts and the number of dependents you have will impact the percentage of your income the IRS can garnish.

In addition to the federal government having this right, state and local governments can also collect unpaid taxes through wage garnishment. State law will dictate how much they can garnish from your paycheck.

Known as an "administrative garnishment," money can be taken directly from your paycheck if you fall behind on your federal student loan payments. The limit on this type of garnishment is 15% of whichever of the following is the lesser amount:

There are a number of circumstances that will lead to the end of wage garnishment. If one of the following occurs, payments for your debt will no longer be taken directly out of your paycheck:

There are federal limits on how much money can be taken from your disposable income when your wages are being garnished.

A certain percentage of your disposable income can be garnished by creditors in some circumstances. Disposable income refers to any money that you have left over after necessary deductions like Social Security and taxes.

The limits for wage garnishment are based on the type of debt. It's worth noting that some states utilize the federal guidelines, while others impose their own. For this reason, it's a good idea to look at what the guidelines are in your state if you're interested in learning how much of your wages can be garnished.

Here are the federal limits on the percentage of disposable income that can be garnished by a creditor:

If you have an unpaid debt that is several years old, you might be wondering if the creditor can still try to get a wage garnishment order against you. Though debts typically only disappear until they're paid and generally don't expire, many states do have statutes of limitations on how long a creditor has to sue you in order to try and collect the debt.

Some debts don't have a statute of limitations, however, including federal student loans.

Federal law dictates that, for ordinary garnishments, a certain portion of your earnings are exempt from wage garnishment. The amount of your income that is exempt is whichever is greater of the two following options:

These rules apply to consumer debts and other ordinary garnishments but don't apply to taxes, familial support, or bankruptcy.

While there are some states that follow the guidelines outlined by the federal government, others have set larger limits to the amount of a person's income that can be garnished through this process. Some states have even prohibited consumer debt wage garnishment. In the following states, your wages can't be garnished for consumer debts:

If a creditor receives a court judgment against you that orders your wages to be garnished, they can continue to do so until the debt has been repaid.

Wage garnishment typically continues until a debt has been fully paid off. This means that it will not automatically stop after a certain number of years.

When you fail to make payments on a student loan that has been funded by the U.S. Department of Education, you might receive a document known as a notice of wage garnishment. You have thirty days to challenge the garnishment or arrange for a repayment plan. If you don't do this, the garnishment will go into effect and will not end until the debt has been paid off.

Yes, wage garnishment can continue for seven years, ten years, or longer. How long you continue to have wages garnished from your paychecks depends on how long it takes for you to pay off the debt in full.

There are a number of things you can do to try and end wage garnishment when you aren't able to settle or pay the debt. We will take a look at your options in the next section.

There are several options on the table if you are motivated to stop a creditor from garnishing your wages under federal law as well as under each state's law.

You might be able to protect some of your wages under your state's laws in certain circumstances. To do this, you'll need to file a claim of exemption with the court in your state. This is a process that entails asking for the creditor's garnishment to completely or partially stop.

Most types of wage garnishments will be immediately stopped when you file for bankruptcy. The reason for this is that there is an "automatic stay order" that will go into place at the time that you file. However, depending on the outcome of the case, this might only be temporary.

Depending on whether you file for Chapter 7 or Chapter 13 bankruptcy, the way the debt will be dealt with varies.

Of course, filing for bankruptcy isn't a decision you want to take lightly. It's also important to understand that several types of debts can't be discharged through bankruptcy. Here are some of the ways that bankruptcy can negatively impact your finances and your life:

Creditors don't need to get a judgment against you before they start taking money directly from your paycheck for certain types of debt, including unpaid taxes and student loan debt. You typically cannot discharge this type of debt through bankruptcy.

If you want to stop the garnishment of your wages for tax debt, there is a process you can go through to negotiate your unpaid tax bill with the IRS.

For student loan wage garnishments, you can request a hearing to challenge the garnishment. There are a number of reasons you might choose to request a hearing, including:

If you are able to pay off the debt in part or in full, that might be the best option for stopping wage garnishment. There are two primary ways you can do this:

Creditors are motivated to recoup the money they are owed, and often would rather receive less money now in a lump sum than the full amount in smaller payments over time.

What this means is that you could be in a good position to settle the debt. You might find that the creditor will be willing to accept a smaller amount of money than the full balance of your debt if you are able to pay it now.

If you are able to come up with the money to pay off the settled amount, you will no longer have to deal with your wages being garnished. Of course, make sure that you receive the deal in writing from the creditor before making the payment.

If you don't stop the debt in some other way or settle the debt, the creditor will likely continue to take money directly from your paycheck. Every time they garnish your wages, the total balance that you owe will be reduced.

That being said, it's important to note that you'll likely also have to pay interest for many types of debt. Depending on your state's laws, the amount of money you owe in interest could vary from 2% to 18% in addition to the principal you owe.

If there is a significant interest rate attached to your debt, this can make it take a lot longer to pay off in full.

Before I sign off, let's take a look at some common questions I receive about wage garnishment.

If you are feeling overwhelmed by the fact that your wages are being garnished, it can be useful to know whether or not you're finding yourself in a unique situation. The truth is, there are more people out there getting their wages garnished than you might initially think.

According to the ADP Research Institute, 7% of employees in their study (which looked at 12 million individuals) had their wages garnished in 2016. This percentage increased to 10.2% for employees between the ages of 35 and 44.

The most common types of debt that individuals are dealing with when they have their wages garnished are:

It's worth noting that there are actually two different types of garnishments to be aware of:

Wage garnishment is when your employer is legally required by a creditor to give them part of your earnings in order to repay what you owe.

Nonwage garnishments, on the other hand, occur when a credit gains access to your bank account. These are also known as bank levies.

As a part of the wage garnishment process, you do have some rights. In most states in the U.S., however, the responsibility to be aware of these rights and exercise them falls on you.

Here are some things you'll want to be aware of if your wages are being garnished or you believe you are in danger of having your wages garnished:

When your wages are being garnished for an unpaid debt, this process will typically continue until the debt has been fully repaid. Though it is difficult to stop wage garnishment once the creditor receives a court order, it isn't impossible. There is often a fairly short window for challenging wage garnishment, so it's important to act quickly once you have received notice.

You also might be able to file an exemption claim depending on the type of debt and the state you're in. It's possible that you'll have to respond to an exemption challenge from your creditor or go to court to present your case.

It is typically best to find an experienced attorney or other expert legal guidance when trying to stop wage garnishment. The truth is, there's a lot of variation between states when it comes to wage garnishment regulations, and they're often quite complicated.

Wage garnishment can have a significant impact on your current and future finances. Not only are you dealing with a reduction of income that can make it even harder to make ends meet, but it can also have a negative effect on your credit scores. Though your wage garnishment won't necessarily show up on your credit report, the series of missed payments that led to the garnishment will.

Are you interested in cleaning up your credit report and setting yourself up for a better financial future? Are you searching for resources to help you on your journey to improve your credit? If so, make sure you check out the rest of our Credit Building Tips blog!

Your credit score doesn't just have an impact on your ability to get a new credit card or take out a loan. It can also make it harder to find an apartment. In this article, we'll tackle the topic of renting with bad credit but high income.

Having bad credit can make your apartment search more difficult, but you'll find it's easier to score the perfect place if your income is high and you have money saved in the bank.

There are a number of tactics you can use to rent when you make good money but don't have great credit. These include looking for landlords that don't run credit checks, offering to pay several months' rent up front, and proving your income and savings to prospective landlords.If you're stressed about finding an apartment with imperfect credit, don't worry. Through some combination of the following strategies, you should be able to sign a new lease in no time.

It's common for potential landlords to take a look at your credit before signing a lease. If you have a high income and are capable of making rent payments but your credit has seen better days, this can be a pretty frustrating reality.

The reason that landlords will commonly check the credit of applicants is that they want to know how likely it is that renters will pay their rent on time, every time.

Your credit history can, therefore, make a big difference in whether or not you score the apartment of your dreams. It's a good idea to check your own credit so you can get a sense of what potential landlords will see when you apply.

They will typically also scrutinize your:

There are a number of different ways that landlords will check your credit, and some will also run a background check. This means that they will probably also be searching for any criminal history or history of evictions.

If your credit is bad but you bring in a healthy salary every month, you have some options. There are a number of strategies you can use to score the apartment of your dreams even when you don't have a pristine credit history.

Thinking about buying instead of renting? Check out our posts about the credit score you need to buy a mobile home, how your credit score impacts the size of your home loan, and whether it's bad to get a new credit card before buying a house.

Perhaps one of the easiest things you can do to rent an apartment with bad credit, regardless of your income, is to look for rentals that don't require a credit check.

How easy it is to find a landlord who won't want to run a credit and background check is going to depend on your location. In some areas where most properties are owned by bigger landlords, for example, you might struggle to find any owners who won't want to look at your credit. In places where there isn't as big of a rental market and smaller landlords, though, you might have better luck.

In general, if you want to avoid a credit check during your apartment hunt, you should look for the following:

Typically, the following types of landlords or properties will require a credit check:

Another thing you can do to find an apartment when your credit is poor is to work with a real estate agent. They'll know the ins and outs of your local market and likely have a good sense of which properties won't require a credit check.

In some markets, it's very common to work with a real estate agent to find a rental.

This typically comes at a cost-- you usually have to pay a finders fee once you sign a lease. This is commonly a percentage of the rent you'll pay for a year. Depending on the rental rate, this can be a substantial amount of money, so you'll want to make sure you understand the fees before signing on with a real estate agent.

When you have a low credit score, it is an indication that you have not practiced responsible borrowing habits. This can be a red flag to landlords who simply want to rent to people who will pay on time and not cause any trouble.

If you have a high income, though, you might be able to show this to a prospective landlord in a way that will help alleviate their doubts about your trustworthiness as a renter.

You might also show them that you have access to a large credit line to help give them a little more peace of mind.

If you have a substantial amount of money saved up, it can be useful to prove this to potential landlords in addition to your high income.

In the best-case scenario, you'll be able to show that your savings account has enough money to cover move-in costs plus three months of rent.

Sometimes, people have bad credit because they have been truly irresponsible as borrowers. In other cases, though, there is a totally understandable reason for a lower-than-ideal score.

If you want to rent an apartment that requires a credit check, it's a good idea to be upfront and honest with the landlord. Having bad credit doesn't mean you're a bad person or a bad tenant, and landlords know this. If you can explain what happened that led to your credit hiccup, they might be willing to work with you.

Depending on the rental market you're in, it might be appropriate to send a letter of explanation along with your application, or it might be better to talk to the landlord in person.

You can also take the time to show your potential landlord that you are actively working to improve your credit. If you send a letter of explanation, you can discuss the concrete steps you're taking and prove that your credit score is already on the rise.

Perhaps one of the most effective strategies you can use to rent an apartment when you have a high income but bad credit is to offer to pay more than just the standard first month, last month, and security deposit.

One of the reasons landlords are skeptical of renting to people with bad credit is they're worried the tenants will miss rent payments. When this happens, landlords are still on the hook for mortgage and operating costs, which puts them in a financial bind. Beyond that, tenants who continuously miss rent payments might end up causing a legal nightmare if the landlord has to pursue an eviction.

If you offer to pay more up front, such as three months' rent on top of the standard first month/last month/security deposit, it will show the landlord that you are financially capable of paying the rent. It also lets them know that you're serious about renting the place and motivated to prove yourself as a good renter.

Beyond that, paying more upfront gives the landlord a bit more protection. They expect to generate a certain amount of income through rent, and knowing that you're paid through the first several months can make them more confident in your ability to pay on time.

Another option on the table is to find a co-signer. Also sometimes called a guarantor, a co-signer is a person that is agreeing to foot the bill if you don't pay your rent on time.

Since this is a pretty big commitment on the part of the co-signer, this role is typically played by a parent or close family member. In order for a co-signer to be useful, they will need to have good credit and, ideally, very good credit. Additionally, they will need to hand over proof of income as a part of the application process.

Landlords will often want to see that co-signers have an income that is at least 80 times the monthly rent.

Before you start looking for a co-signer, it's important to consider the potentially negative implications of this type of partnership. Mixing family and money can be a tricky business, and if you fail to pay your rent and your co-signer is forced to take responsibility for it, there's a good chance it will cause tension and strife. You never want to take on a co-signer for something you can't reasonably afford, so this is something you'll want to consider seriously before going this route.

Finally, another step you can take to score an apartment with bad credit but a high income is to consider renting with a co-tenant. Of course, it's essential that this co-tenant has good credit; otherwise, it won't help you prove your case as a responsible renter.

Not everyone is thrilled by the idea of living with a roommate, but this can be a good option if none of the others are working for you. You can save money by splitting your housing costs with another person while you work to build your credit. With attention and dedication, you'll eventually be able to rent a place of your own.

Credit scores and credit reports can feel pretty abstract a lot of the time, but the truth is that they can have a huge impact on the quality of your life. If you want to rent an apartment, for example, having bad credit can make the search much more difficult and limit your options.

That being said, having bad credit with a high income does give you some advantages compared to having bad credit with a low (or no) income. With some money coming in every month and money in the bank, you'll likely find there are some landlords out there who are willing to work with you.

If you're thinking about renting an apartment soon, but you're worried about your bad credit, it's a good idea to start working to build your credit now. For more resources about how to improve your credit and open up more financial opportunities for yourself in the future, make sure you check out our Credit Building Tips blog.

If your credit card account is paid off in full and you initiate a refund, how does it work? What happens if you get a refund on a credit card with a 0 balance?

Credit card refunds don't work in the same way as cash or debit card refunds because it's actually the card issuer that paid the merchant or vendor, not you. This means that you won't receive the refund in cash, but instead as a credit to your account.

If you have paid off your balance in full before a refund is issued, you will have a negative balance on your account. The next time you make a purchase using your card, this credit will be used first. If the refund is for a substantial amount of money or you don't intend to use that credit card again, you might be able to ask for the money to be sent as a check.Let's take a closer look at what you need to know about credit card refunds and what to expect when you have a negative balance on your account.

If you buy something using a credit card and then later return it, you won't be able to get your money back in cash. What will happen instead is that you'll receive a credit on your account. The credit that you'll receive will be equal to the amount of the original purchase.

Typically, the refund process will start once the merchant has agreed to accept your return and issue you a refund. However, if the person you bought the item or service from refuses to give you a refund or is unable to, it's possible you can utilize your return protection.

In order to determine whether or not your circumstance qualifies for return protection, you'll want to contact your credit card issuer. They will be able to help you understand the protection policy associated with your card.

Understanding how credit card refunds work requires that you first understand the steps involved in processing a transaction.

When you buy something using your credit card, you aren't actually the one that is paying the merchant. Instead, the credit card company is.

Once the purchase has been made, you'll see your available balance go down on your credit card account. When you make payments to pay down your credit card balance, you're paying the credit card company back for the money they lent you for purchases.

Also involved in the process are credit card networks. These are companies that act as a mediator between merchants and credit card issuers in order to process payments. Before you can receive a refund for your purchase, the merchant has to send the refund to the credit card company.

It is for this reason that you can't use another payment method to receive a refund for a credit card purchase (i.e., receiving the refund in cash or putting it on another card). Similarly, this is why it can often take a number of days to receive a credit card refund.

It will typically take several days in order to see the credit appear on your account after a refund. This is because the return has to go through a specific process via the credit card networks.

There are three key methods that will determine precisely when you can expect your refund to show up, which are:

For example, you might find that you receive credit for your refund more quickly if you are returning the item in person. In general, though, it will take between five and fourteen business days to see the credit show up on your account.

If you want to have access to the refund money as quickly as possible and you expect to make another purchase from the same merchant, one alternative is to ask for store credit. However, it's important to understand you will still owe the credit card issuer the money you have used for the original transaction.

Let's say you made a purchase on your credit card, and you have since paid down the account balance to $0. If you then go to return that item, what will happen to the balance on your account?

Usually, this will result in having a negative balance on your account. Basically, the credit card issuer will owe you money rather than the other way around. The next time you make a purchase, this negative balance will be used first.

For example, let's say you have a $0 balance, and you return an item with an original purchase price of $50. Once the refund is credited to your account, you will have a balance of negative fifty dollars.

If you were then to purchase something else for $50 using that same card, your balance would return to $0, and you wouldn't owe the credit card issuer any money. If you were to purchase something else for $100 using the same card, your balance would be $50 after applying the negative balance.

While this usually isn't a problem so long as you regularly use this particular credit card, you might be wondering what you can do to have access to your funds if you don't plan on using the card anytime soon. For a particularly large negative balance or a card you rarely use, you can ask the issuer to send you a check in the amount of the negative balance.

The word 'negative' in the term 'negative credit card balance' makes it sound like it's a bad thing. In actuality, having a negative credit card balance means that you owe less than nothing to the credit card company-- they actually owe you money.

This can occur for a few different reasons, the most common of which are:

There's nothing wrong with having a negative balance on your card. The next time you use your card, this credit will go toward the purchase price before you owe the credit card company any more money.

However, you can request a deposit if you don't want the credit sitting in your account unused. Usually, a credit card issuer will be willing to send you the money through direct deposit to your bank account, a check, or a money order.

Before I sign off, let's take a look at some of the most commonly asked questions about credit card refunds.

Some credit card issuers offer credit card return protection. This is a perk that allows cardholders to make a return even when the merchant won't allow it. Even if the retailer does allow returns, having a card with return protection can extend the period of time you are eligible to return an item.

This is, unfortunately, a perk that is less and less common. Many issuers have recently been phasing out this type of benefit. For that reason, you don't want to assume that your card has return protection and instead should look closely at the details of your card agreement and benefits.

Money can be returned to a cardholder through both refunds and chargebacks. However, these two processes occur for different reasons and aren't exactly the same in their process.

If you want to return something and receive credit on your account, you will have to go through the merchant. There are typically parameters you have to follow in order to return an item for a full refund, and these are set by the merchant themselves.

If you want to get a credit card chargeback, you will go through your credit card issuer. To do so, you'll have to dispute the particular transaction with your credit card company. They will then initiate a chargeback with the bank of the merchant, and the merchant will have to prove that they provided the described product or service to you. If this evidence can't be provided, you will usually be granted the chargeback and see the disputed amount show up as a credit on your account.

When you initiate a chargeback, you are disputing a purchase that has already been charged to your credit card account. Rather than being paid directly from the vendor or the merchant, a chargeback is processed by your bank or credit card issuer.

There are a number of different reasons you can choose to use the chargeback process. These include:

Going through the chargeback process can actually be pretty time-consuming. The merchant can end up owing the credit card company if the dispute is ruled in the cardholders favor. For this reason, many merchants prefer to simply have generous return policies rather than facing the chargeback process while also potentially alienating a customer.

Being refunded after you return an item or are displeased with a service is a fairly straightforward process. For most people, receiving a credit on their credit card balance is just as good a method of receiving their refund as any other.

That being said, there are a few disadvantages to be aware of when initiating a refund for a purchase made with a credit card.

Do you use your credit card rather than other payment methods in order to benefit from the points or perks you earn? If so, you'll want to know that you'll likely lose the points that were earned on the particular purchase if you initiate a return.

As the cardholder, you'll be expected to return any reward points that are associated with the money used for the purchase. This doesn't just have to do with cash back or travel miles, either-- it also applies to sign-up bonuses and other spending-based incentives.

For example, let's say that you have to spend $2000 in the first four months of opening your account in order to receive a promotional sign-on bonus. If you make a $500 purchase toward the end of this period so that you qualify for the bonus, you'll want to understand that you'll lose the bonus if you were to return the same $500 purchase.

If you are returning a foreign purchase, it's worth understanding that you'll probably get stuck with any foreign transaction fee. The reason for this is that it costs your credit card issuer money when you make an international purchase.

Credit card companies need to process international purchases through currency market purchases. In order to allow you to buy the item or service originally, they took on additional costs.

The specific terms, however, will ultimately vary depending on your credit card issuer and the card itself. It never hurts to ask, at the end of the day, as it's possible your issuer will be willing to send you a refund for foreign transaction fees via statement credit. You will generally have an easier time of this if currency values haven't fluctuated significantly since the time of purchase and if you swiftly made the return after purchase.

When you purchase a product or service that you want to return, the first step is to contact the company that sold it to you. Ask them if they will reverse the charge. Depending on the circumstance, they might ask that you return the product to them.

If the merchant's response isn't satisfying to you, it's possible you will be able to dispute the charge. To dispute a charge, you'll want to contact the credit card company associated with the account you used to make the purchase.

This process is known as a chargeback. Card issuers will sometimes offer protections if you received a defective item or if you otherwise didn't receive the goods or services you purchased.

It's also possible that you may be granted the right not to pay the remaining balance on a purchase if you only paid part of a bill for a product or service that you purchased with the card. In order to be considered for this type of chargeback, you will typically need to meet the following criteria:

Another important question to answer is whether credit card refunds count as a payment. After all, if you have a minimum payment of $50 and you received a statement credit for $50 due to a refund, you're probably wondering whether you're still on the hook for your minimum payment this month.

Usually, getting a refund to your credit card counts as an account credit doesn't count toward your minimum payment. Though it would be nice if it was viewed as a payment by the issuer, this is not the case.

This means that you'll still be responsible for making your minimum monthly payment even if you receive a refund equal to or larger than that amount. Otherwise, you could get hit with a late payment fee and even a mark on your credit report if you don't quickly remedy the issue.

When you receive a credit card refund, it will usually help to reduce your total outstanding balance. This means that a refund is generally a positive thing for your credit score. There are a number of factors that impact your credit score, but one of the most significant factors is "amounts owed." When either your FICO score or VantageScore is calculated, 30% of your score results from this category.

For example, let's say that you have a credit limit of $2,000 and the balance on your card is $600. This would mean you have a credit utilization ratio of 30%, which is just about as high as experts suggest you let your credit utilization get.

What happens, though, if you make a return and receive a $200 refund? This would mean that your balance goes down to $400, reducing your credit utilization to 20%. When it comes to credit utilization, lower is always better, and keeping your balances low in relation to your credit limit is a great way to maintain a healthy credit score.

If you initiate a return for a purchase you made with a credit card, the merchant will first have to agree to send a refund. Since it was actually the credit card company that paid the merchant on your behalf, the money will be sent to your credit card issuer, not directly to you. This means that you will end up with a credit on your account.

If you have already paid off your account balance in full, this will result in a negative balance. The next time you go to make a purchase, this credit will be used first before you start racking up a positive balance.

For some refunds, the dollar amount might be large enough that it isn't ideal for it to be sitting as a credit in your account. In these cases, you might be able to ask the credit card company to send you a check in the amount of the refund.

Similarly, if you don't plan to use that credit card in the near future, the issuer might be willing to send you the funds in cash. If they go unused for a certain amount of time, it's possible they will send you the check unsolicited.

Are you on a mission to improve your credit and increase the financial opportunities available to you? If so, make sure you check out our Credit Building Tips blog for more resources, guides, and helpful tips.

Credit card application questions will ask you a series of questions when you apply online. What if you accidentally put the wrong income on your credit card application? Are there any potential repercussions?

The truth is that credit card companies do not typically verify the income of every applicant. This would simply be too costly and time-consuming, given how many applications they receive on a daily basis.

At the same time, it's important to understand that a credit card application is considered a legal document. This means that you are exposing yourself to a number of potential consequences when you misrepresent your income.For this reason, it's a good idea to provide accurate information on your application. If you accidentally entered the wrong income, the safest bet is to change your income using your online account or call your card issuer to explain what occurred.

Lying about your income when applying for a credit card is considered fraud-- specifically known as loan application fraud. This is a crime that can come with some pretty substantial penalties, including fines and even time in jail.

You are signing a legal document when you apply for a credit card. For this reason, it's important to make sure you are reporting your income accurately.

Even though this sounds pretty scary, the truth is that it's pretty unlikely to be convicted for loan application fraud for misreporting your income on a credit card application. This is particularly the case if you only made a small error when it comes to reporting your income.

At the same time, people will occasionally be prosecuted for loan application fraud. For example, a particularly egregious case involved a Minnesota man who committed loan application fraud to the tune of nearly half a million dollars, immediately filing for bankruptcy right after he collected his last payment. For his crimes, he was ordered to pay more than $700,000 in restitution and spend 57 months in federal prison.

Major credit card issuers are likely receiving tens if not hundreds of thousands of applications on a daily basis. Despite their sizeable workforce, this makes it impractical to analyze each application closely.

Typically, it isn't worth expending the required resources for a credit card company to verify your income. Financial institutions will, however, ask for proof of income when the stakes are much higher, such as taking out a mortgage or another large loan.

Not quite sure what counts as income when applying for a credit card? Check out our guide to properly reporting income on credit card applications.

In some cases, credit card companies might ask you to submit pay stubs or bank statements in order to verify your income. However, they aren't going to be able to look at your bank account information without you giving them permission. How much money is in your bank account also won't appear on your credit report.

What credit card issuers will be able to see when they do a hard pull of your credit is your credit history. This will help them understand how risky you are as a borrower, which basically means how likely you are to pay back debt on time.

You can get free copies of your credit reports from AnnualCreditReport.com. By checking your credit reports, you can see what potential creditors will be able to see when they do a hard inquiry into your credit.

Even though credit card companies won't have easy access to your income or how much money you have in your bank accounts, you still don't want to overstate your income on your application. Issuers can sometimes ask applicants for proof of income randomly, and you could end up having your application rejected if your reported income doesn't match the proof you provide.

You will also draw more attention to yourself if you start falling behind on your payments. Financial institutions might investigate why you are being offered a credit limit you don't seem to be able to keep up with. For instance, American Express is known for watching out for red flags that can lead to an audit and a locked account. When this happens, borrowers won't be able to use their credit anymore until income verification or other data is provided.

Applying for a credit card these days is a very simple process. They'll typically ask you for personal and financial information, including your:

As you might imagine, having a higher income can help improve your chances of being approved. Beyond that, this can also lead you to receive a higher credit limit.