As of this month, there are 212 companies offering credit cards. But if your credit score is fair or poor, it may take a lot of work to get approved for one.

With low fees, store credit cards can be a great way to build credit if you are trying to establish credit or rebuild credit if your score has taken a hit for whatever reason. That's just one perk of getting a store credit card. Most store cards offer retailer discounts and membership perks.

When it comes to department stores, even though their numbers may be dropping across the country, they are still the anchor stores in many malls. And along with offering a wide range of products from fashion and fragrance to bedding and bath sets, almost all department stores also offer store credit cards.

The two most common store cards are "open- and closed-loop" cards.

Although store cards have a reputation for inflicting high-interest rates and hidden rates on their customers, they can offer special financing on big purchases and let you earn rewards and discounts at your favorite store.

To help you make decisions before you reach the checkout aisle, we've compiled a list of the best store credit cards to get, even if your credit score is under 600!

To help you make decisions before you reach the checkout aisle, we've compiled a list of the best store credit cards to get, even if your credit score is under 600!Card details: The TJX Rewards® Platinum Mastercard® can be used at T.J. Maxx, Marshalls, HomeGoods, Sierra Trading Post, and Homesense. It's ideal if you often shop at this family of stores, but it can be used anywhere Mastercard is accepted.

Pros:

Cons:

Card details: This card is worth considering if you plan to spend up to $1,667 at the store in the first two days of having the card, as you can earn 15% off all purchases. The discounted savings is capped at $250.

Pros:

Cons:

Card details: You can qualify for the Kohl's Credit Card with a lower-than-fair credit card score if your income, debt load, opening of accounts, employment, and housing status are higher.

Pros:

Cons:

Card details: The JC Penney credit card is a department store credit card that can only be used at JC Penney. It doubles the rewards rate of a standard JCPenney rewards member.

Pros:

Cons:

Card details: Citibank, N.A. issues the Macy's credit card that can be used at Macy's, Macy's Backstage, and macys.com. It's available in four levels — Bronze, Silver, Gold, and Platinum, each with increasing benefits.

Pros:

Cons:

Card details: The Montgomery Ward retail card is an unsecured store credit card that even people with bad credit can get. They report to the credit bureaus monthly, so if you make on-time payments and have a reasonable credit utilization rate, you'll be able to build a positive credit history.

Pros:

Cons:

Card details: The BJ's Perks® Mastercard® lets you add authorized buyers to share your credit card and membership number. One authorized buyer can be added when you apply for the card, and three additional authorized buyers can be added once your account is opened.

Pros:

Cons:

Although not technically department stores, these four stores (big box, home improvement, catalog/online retailer, and clothing store) will also extend credit to those with lower or bad credit scores.

Card details: If a significant amount of your shopping for groceries, garden supplies, new clothes, or other everyday items is done online at Walmart, the Capital One® Walmart credit card provides great rewards.

Pros:

Cons:

Card details: This in-house store credit card can only be used at Lowe's, a home improvement retailer that sells building supplies, hard finishes, and appliances.

Pros:

Cons:

Card details: This is the store credit card that's easiest to qualify for with bad credit. Not technically a department store; it's an online retailer/mail catalog store.

Pros:

Cons:

Card details: The Old Navy credit card can be used at Old Navy, Gap, Banana Republic, and Athleta. When you shop at two or more of these stores, you can earn up to 2,000 bonus points.

Pros:

Cons:

When your credit score is lower than you'd like it to be and you can't find a department credit card that suits your style, two other types of credit cards may extend your credit and help you build up a higher credit score.

In the main, secured credit cards work like conventional credit cards. The main difference is that secured credit cards require you to give an upfront cash deposit that acts as collateral against the card's future use.

Student credit cards are a great first step to building credit as they don't rely on someone's previous credit history or income before approving the card. Most student credit cards don't offer rewards, but the SCENE® Visa* card for students and the L'earn® Visa* card do.

The SCENE card lets you earn five Scene+ Points for every $1 spent in Cineplex cinemas and one Scene+ Point for every dollar spent elsewhere. Using the L'earn card lets you earn 1% money back on all "eligible" purchases.

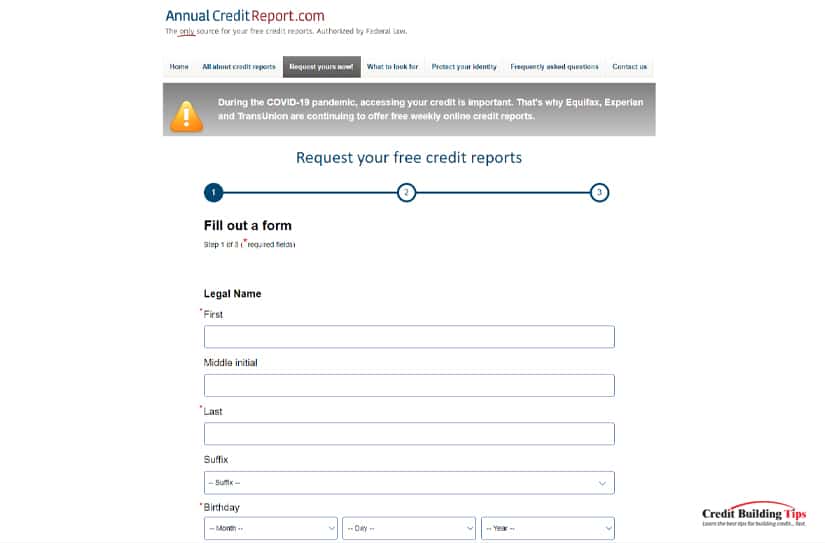

Credit bureaus update information sent by lenders every 30-45 days. If any changes are made to your financial behavior, like how many credit accounts you have and your payment history, your report will reflect the updated information.

Due to COVID-19, AnnualCreditReport allows you to get your credit report for free until the end of 2023. After that, you'll be able to check your report for free once a year.

It's important to check your credit report for errors, as these can negatively impact your score. It also benefits you by helping you understand what future lenders see and what specific activities (how you pay your bills, what types of credit you use, your credit utilization ratio, etc.) you need to do to improve your score.

How you pay your bills — your payment history — makes up 35% of how your credit score is calculated. This is why it's important to pay all your bills on time. The more on-time payments you make, the higher your credit score will be.

Payment history considers if you pay your bills on time, if and how often you miss a payment due date, how far past the due date your payment was made, and how long it's been since you missed one or more of your payments.

Of course, paying your credit card bills fully helps your credit health. To create a healthy credit report, you need to make at least the minimum payment on each credit card.

But if that's all you pay, you will incur hefty interest charges on top of any unpaid balance you owe. The cost of one $30 sweatshirt, if you make only minimum payments over a year, can end up costing you $300+ by the time you've paid it off in full.

Repaying your balance in full and on time every time is one of the best ways you can move a low credit score to a higher one. This will make you a more attractive loan recipient from lenders offering you better borrowing terms.

When working hard to improve your credit score, you may want to consolidate your credit card debts if you have multiple cards with high balances you find difficult to pay off.

For example, if you have four credit cards with varying balances between $800 and $1,400, you may need help remembering to make the four separate payments on time. A consolidation loan to cover the entire credit card debt amount would let you have one single amount owing at a lower APR, which will lower the interest you'll have to pay.

This may not seem obvious, but calling your credit card company can change how your credit mistakes are reported to the three main credit bureaus — Experian, TransUnion, and Equifax.

Yes, you'll need to go through the painful phone tree or wait endlessly on hold while you listen to elevator music, but remembering that a single late payment can cause your credit score to drop by 90-110 points should help ease the irritation.

Once you get through to a human being, an honest and reasonable explanation for why you were late (your payment was made by mistake) can set the stage for them to extend a little bit of helpful mercy. Tell them you're doing everything you can to build a good credit report, and ask if they would consider removing the late payment from your record.

A polite and sincere request can help your case and, along with a commitment to developing good credit habits in the future, should move your credit score in the right direction.

Do You Get Cash Back With a Credit Card at a Grocery Store?

Do You Get Cash Back With a Credit Card at a Grocery Store?

FAQ: Which American Express Credit Card is The Easiest to Get?

FAQ: Which American Express Credit Card is The Easiest to Get?

Are There “Guaranteed Approval” Credit Cards for Bad Credit?

Are There “Guaranteed Approval” Credit Cards for Bad Credit?

Is Amex Platinum Worth The $695 Annual Premium?

Is Amex Platinum Worth The $695 Annual Premium?

When Does AirBnB Charge Your Credit Card? [Plus FAQ]

When Does AirBnB Charge Your Credit Card? [Plus FAQ]

Why Do People Use Credit to Pay for Things Instead of Cash?

Why Do People Use Credit to Pay for Things Instead of Cash?