When you have a less-than-ideal credit score, it can mean that you have to pay higher interest rates when you borrow money or that you struggle to even be approved for credit. Considering how important it is to have a solid credit score, it’s worth having a fairly thorough understanding of not just what helps your credit score but also what hurts your credit score.

Though there are a number of different credit scoring models that can be used to calculate your precise score, the most common models consider similar factors including your payment history, credit utilization, credit history length, and more.

Things like missing just one bill payment, keeping high balances on your card, or closing old accounts can all have a negative impact on your score.

Things like missing just one bill payment, keeping high balances on your card, or closing old accounts can all have a negative impact on your score.Let’s dive in and take a closer look at some of the surprising things that can damage your credit score to help you keep your score as high as possible.

Before we can take a look at what hurts your credit score, we first need to explore how your credit score is calculated. By understanding the different factors that influence your credit, you can get a better sense of how to keep your score healthy and high.

There are two primary entities that calculate consumer credit scores (FICO and VantageScore,) both of which have several different models that have been released over the years. Furthermore, there are some industry-specific credit scoring models that might be used by lenders. This means that you don't actually have one sole credit score but potentially several.

Each of these models consists of its own particular formula for calculating consumer credit scores. In general, though, you can expect the following factors to have an impact on your score.

Your payment history is the record of your payments on credit accounts, including credit cards, mortgages, and other loans.

On-time payments positively affect your score, while late payments, defaults, and bankruptcies can have a negative impact.

Your credit utilization is the ratio of your current credit card balances to your credit limits.

Maintaining a low credit utilization ratio (using a small percentage of your available credit) is generally considered favorable for your credit score. Most experts recommend that you keep it below 30%, but the general rule is that lower is always better.

The length of time you've had credit accounts is also considered when determining your credit score.

Generally, a longer credit history shows creditors that you have ample experience managing debt, which reflects favorably in your credit score. This factor usually involves looking at the age of your oldest account, the age of your newest account, and the average age of all your accounts.

Opening several new credit accounts in a short period can be seen as a risk, especially if you don't have a long credit history. Each time you apply for new credit, a "hard inquiry" is made, and this can slightly impact your score.

If you apply for a bunch of different credit cards or loans all at once, it looks to lenders like you might be hard up for cash. This reasonably makes them nervous that you are overextended and going to struggle to actually pay back the money you are borrowing. For this reason, too many new credit accounts can ding your score a bit.

The "types of credit" factor considers the variety of credit accounts you have, such as credit cards, mortgages, installment loans, and retail accounts. Having a mix of different types of credit can be positive for your score. Though your types of credit in use only usually count for about 10% of your score, the positive benefits of having a diversity of credit account types are still worth keeping in mind.

There are also a number of factors that you might expect to impact your credit but actually don’t have any influence over your score. By understanding what doesn’t affect your scores, you can get a better sense of what to prioritize when working to improve your credit.

Some things that won’t help or hurt your credit include:

What else won't impact your credit score? Here are a few other things that might surprise you:

When it comes to maintaining a healthy credit score, knowledge is power. Understanding what hurts your credit score is just as important as understanding what helps your score. After all, even one little slip-up can have a negative impact on your creditworthiness in the eyes of potential lenders.

As discussed above, payment history is a crucial component of your credit score. You might think that it’s not a big deal to miss one payment, but the truth is even one missed payment can damage your score.

Missing even one payment can impact your credit score and have other negative repurcussions. For example, you will likely be charged a late fee and might be saddled with a penalty interest rate. If you continue to miss payments, your account may be referred to a collections agency, which can pursue you for the outstanding debt.

For this reason, it’s essential that you always at least make the minimum payments on your debts. Setting up autopay is a great strategy for ensuring you’re not relying on your memory to pay your bills on time.

If you have decent credit, there’s a good chance you regularly receive pretty enticing credit card offers with some regularity. While there isn’t anything inherently wrong with benefiting from the rewards offered by different credit cards, it’s important to recognize that seeking too much new credit at once can hurt your score.

A hard inquiry, also known as a hard pull, occurs when a lender or creditor checks your credit report as part of their decision-making process for extending credit. This typically happens when you apply for a new credit card or a loan (such as a mortgage, auto loan, or personal loan). A soft inquiry, also known as a soft pull, occurs when someone checks your credit report for a non-credit-related reason. These inquiries do not impact your credit score.

The reason for this is that every new credit application is going to result in a hard inquiry into your account. Your score can temporarily drop if you apply for a number of new accounts in a short span of time, which can be a problem if you’re trying to lock down the best rates and terms for a loan.

Paying off debt can be an incredible, freeing feeling. It’s tempting to close your credit card accounts once you’ve paid your final bill, but it’s a good idea to think twice about this. Closing credit card accounts can hurt your score in a few different ways:

Lots of parents want to help their children in any way they can, and one common method is to co-sign on a loan. Furthermore, it can be tempting to help out a close relative or friend who is struggling to receive a loan on their own.

A co-signer is an person who signs a loan or credit agreement alongside the primary borrower and agrees to take responsibility for the debt if the primary borrower is unable to make the required payments. Co-signers are often used to help individuals who may not qualify for a loan or credit on their own due to a lack of credit history, a less than ideal credit score, or insufficient income.

There’s nothing wrong with co-signing a loan, but it’s important to consider all of the potential consequences before moving forward. If the person you’re trying to help out ends up defaulting, your credit score can suffer. Additionally, mixing money and personal relationships has a tendency to get pretty messy, so make sure you have a clear (written) understanding between the two of you in terms of how you will deal with all of the details of the loan.

Becoming an authorized user on another person’s account can actually be a great way to build credit or improve an imperfect credit score.

An authorized user is a person who is given permission by the primary account holder to use their credit card. While authorized users can use the credit card to make purchases and transactions, they are not legally responsible for the debt incurred.

At the same time, though, you want to be very careful when you sign on as an authorized user, as it won’t do you much good if the primary user keeps high balances or misses payments. In fact, if they aren’t responsible credit users, it can end up hurting your credit.

Having too many credit cards can be stressful, and consolidating your debt through one credit card or loan can be incredibly convenient. At the same time, transferring all of your balances to one card or loan could potentially impact your credit.

Though your credit mix isn’t the biggest factor that impacts your score, it’s still a good idea to have a few different types of accounts in your credit report. The two primary types of credit are revolving and installment.

Revolving credit includes credit cards and HELOCs– essentially, these are lines of credit where you are offered a certain credit limit you can borrow against. Installment loans, on the other hand, involve receiving a lump sum that you pay back over time in regular installments. Examples include student loans, auto loans, personal loans, and mortgages.

Having access to credit can be a great thing, but you definitely don’t want to be maxing out your cards every month. Even if you’re doing a good job making minimum payments on time, you might see your credit score drop if your credit utilization keeps going up, thanks to monthly interest charges increasing your balance.

A little less than a third of your credit score is determined by your “amounts owed,” of which credit utilization is a part. Experts typically recommend keeping your credit utilization at 30% or lower. You can determine your own credit utilization ratio by adding up all of your credit balances and dividing them by your overall credit limit.

While some people struggle with taking on too many new credit cards and damaging their scores through hard inquiries, others stay away from borrowing money to keep themselves free from debt.

While living a debt-free life isn’t a bad thing, it isn’t necessarily a good idea to avoid using credit cards or borrowing money entirely. If the day does come when you want to buy a house or a car, there’s a good chance you’ll want to finance the purchase. Without any credit history, you’re likely going to face an uphill battle in finding someone to lend you the cash.

If you’re considering declaring bankruptcy, it likely means that you have fully exhausted all of the other options on the table when it comes to paying back your debts. While your credit score might not be your biggest concern at the present moment, the truth is it’s worth considering just how damaging bankruptcy can be to your future borrowing options.

There are several different types of bankruptcy, but the two most common types– Chapter 7 and Chapter 13– will show up on your credit report for many years. For Chapter 7 bankruptcy, the negative mark won’t disappear for ten years, while Chapter 13 bankruptcy will stay on your report for seven years.

If you strike a deal with a creditor to pay less than you owe in order to settle, it’s worth knowing that this can impact your credit score. At the same time, in many cases, dealing with your unpaid debt is worth it, even though it can have repercussions for your score.

If your home is foreclosed, this info will stay on your credit report for seven years from the first missed payment date. After bankruptcy, foreclosure is seen as the most serious negative event you can have in your credit file.

If you stop making payments toward your debt or even fall a little behind, your loan or credit account will eventually become delinquent. If your account remains delinquent for a while– usually between 120 and 180 days– the creditor might write your account off as a loss. This is known as a “charge-off.”

You might think that this means you aren’t on the hook for the money you owe anymore, but that, sadly isn’t the case. Instead, the account will likely be sold or assigned to a debt collector, who then tries to get you to fork over what you owe.

Having an account charged off and sent to collections is likely going to hurt your credit score. This information can stay on your credit report for up to seven years.

It’s not just credit card debt and loans you have to worry about when it comes to your credit score. It might seem a bit unfair, but the truth is that paying the child support you owe on time likely won’t help your credit, but failing to make your payments can hurt your score.

Like most other types of negative info, unpaid child support payments can remain on your credit report for up to seven years.

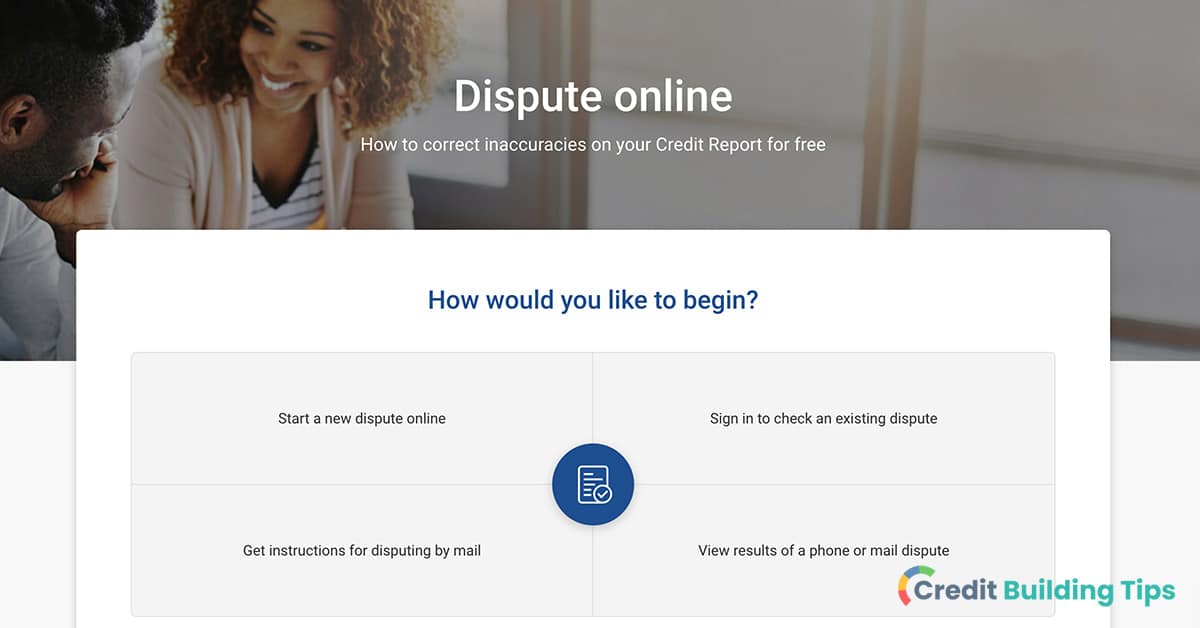

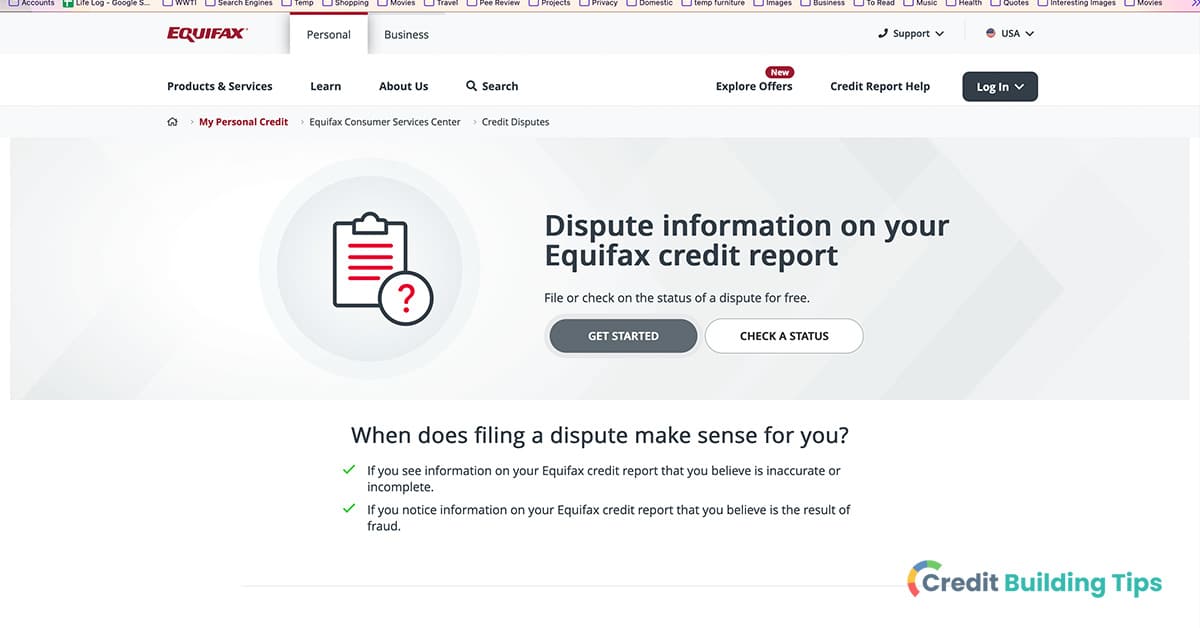

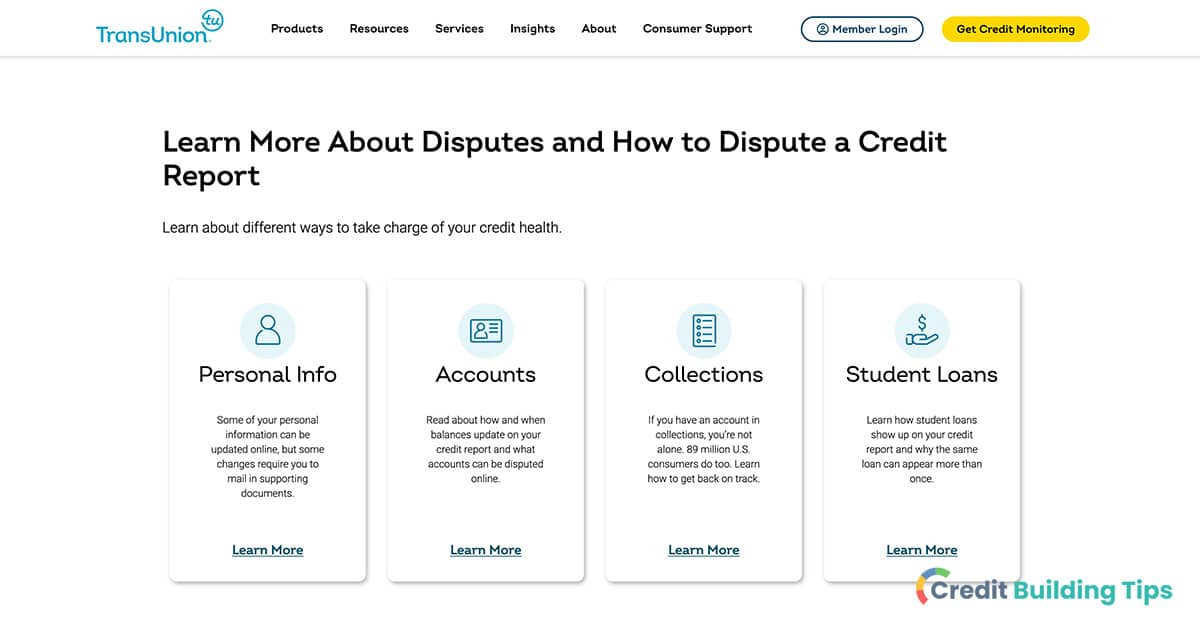

Even if you’re doing absolutely everything right, it’s possible that there is some information on your credit report that is dragging down your score. Errors are not uncommon on credit reports, whether they result from a mistake on the part of the creditor or identity theft.

You shouldn’t assume that everything is hunky dory with your credit report– make a habit of checking it regularly. If you happen to notice an error, you’ll want to start the dispute process right away.

The importance of having good credit can feel pretty abstract until you are actively trying to get a credit card or take out a loan. At the same time, it can be hard to improve your score overnight– building and improving credit typically takes time.

For this reason, it’s a good idea to stay on top of your credit health by avoiding things that can hurt your score and practicing responsible borrowing habits. For more information about how to keep your credit in tip-top shape, make sure you check out our Credit Building Tips blog!

A bankruptcy discharge releases an individual from their legal obligation to repay a debt. This is a permanent order that prohibits creditors from taking any more collection action against the debtor.

Though bankruptcy is often seen as a fresh start for debtors, it doesn't mean that your slate will be wiped completely clean. Both the bankruptcy itself and the discharged debt will show up on your credit report.

Is there anything you can do to remove discharged debt from your credit report? How do you remove incorrect information from your credit report about discharged debt after bankruptcy?

Is there anything you can do to remove discharged debt from your credit report? How do you remove incorrect information from your credit report about discharged debt after bankruptcy?In this article, we'll take a closer look at everything you need to know about forgiven debt after bankruptcy and what it means for your credit file.

If a debt is discharged, it means that you aren't liable for the debt anymore. Beyond this, the lender or creditor isn't allowed to try and receive the money that is owed.

Essentially, debt discharge is the cancellation of a debt. This occurs via the process of bankruptcy.

The people that file for bankruptcy (often referred to as "debtors") will commonly go through this process to remove their obligation to pay certain kinds of debt and obtain a fresh start financially. Though not every single type of debt is dischargeable, most typical consumer debts are dischargeable.

It's possible for taxable income to result from debt discharge unless there are certain conditions met as defined by the IRS.

Discharged debt can result from bankruptcy rulings. If the debtor meets all of the court's criteria in Chapter 7 or Chapter 11 bankruptcy, the court might discharge the debt.

A person or company that has a debt discharged by a court doesn't have to pay back the debt anymore and the lenders aren't allowed to try and make attempts to collect the debt.

Unless the forgiveness is a bequest or a gift, a debt discharge is often something that results in taxable income. If the debtor meets the requirements laid out by the IRS, however, some debt discharges are exempt from paying taxes.

A person that is filing for bankruptcy is trying to eliminate as much of their debt as they can. This allows them to start over financially.

Either immediately or at the end of the bankruptcy process, a number of types of debts will be discharged. The following are some of the types of debts can be discharged:

In Chapter 13 bankruptcy, some additional types of debt are eligible for discharge, including:

Though there can be specific exceptions, there are certain types of debt that typically aren't allowed to be discharged through the bankruptcy process. These debts were deemed to be not eligible for discharge by the U.S. Congress for reasons of public policy:

Qualifying for discharges for these debts is usually very hard to do. You will need to prove that you wouldn't be able to maintain a minimal standard of living if you continued to make payments. You also usually can't discharge penalties and fines from government agencies that resulted from breaking the law, or debts resulting from a drunk driving incident that resulted in personal injury debts.

Other debts that are unlikely to be discharged include:

If you've gone through the bankruptcy process and some of your debts have been discharged, this information will typically show up on your credit report. They can stay on your reports for a long time, which can have a negative effect on how lenders view your creditworthiness.

Technically, you are not supposed to be able to remove accurate information from your credit report. For this reason, there is no guarantee that your attempts to remove correct debt discharge information will be successful.

If the debt discharge is showing up in error or the information regarding them is incorrect, you will definitely want to dispute the information. Any inaccurate information on your credit report should be disputed so that your financial opportunities aren't harmed by incorrect data.

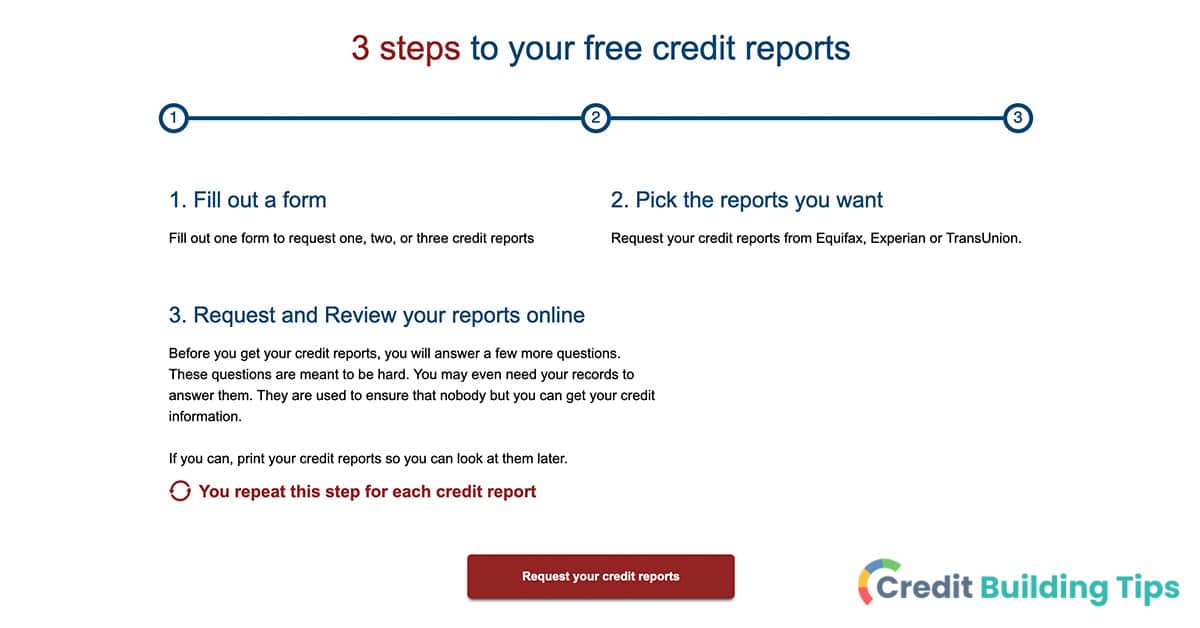

The first step is to review each of your credit reports, which you can get for free from AnnualCreditReport.com. Take a look at your accounts and locate all of the information about the discharged debt that you believe is inaccurate.

Before you file a dispute, it's worth doing some sleuthing to make sure that the information is actually incorrect as you think it is. Take a look at your own records and compare them to what you see on your credit report.

You will want to file disputes with every credit bureau that is reporting inaccurate information. You can do this online, over the phone, or through the mail.

Unfortunately, you won't receive an answer right away-- it will usually take 30 to 45 days to hear the results of the credit bureaus' investigation. Hopefully, they will find, as you have, that the information is incorrect and should be altered or removed. If they don't rule in your favor, though, you can shift your focus toward rebuilding your credit through other means.

Cleaning up your credit report can take time, and some information you will have to wait to fall off your report if it is accurate. Make sure you check out our guides to removing collections, dispute comments, evictions, and late payments if you are ready to improve your credit.

After bankruptcy, there are a number of errors that can appear on your credit reports when it comes to discharged debts. Let's look at some of the most common errors to help you understand what steps you should take.

If you had a debt that was discharged as a result of bankruptcy, it should be noted as "discharged in bankruptcy" or something along those lines on your credit report. The balance due, regardless of how much you originally owed, should read $0.

If you go through all of the trouble to have your debts discharged and your credit report states that you still owe your creditor, it's natural to be surprised and disturbed.

It's possible that your credit report hasn't been updated yet-- if the debt discharge only recently occurred, this is likely the case. Otherwise, you can dispute the information either with the creditor or the credit bureaus to make sure that your report accurately reflects the new debt amount-- zero.

When you have a debt discharged through bankruptcy, it completely severs the relationship that you had with the creditor or lender. This party no longer has any legal right to try and recoup the money you owe and they also don't have any legal right to pull your credit every month.

When lenders do a hard inquiry into your credit, it will bring down your credit score. You'll want to dispute these inquiries in order to have them removed from your report.

Creditors can choose to charge off a credit card account for a number of reasons. However, they are not allowed to do this if you've received a debt discharge or filed for bankruptcy. When a charge-off shows up on your credit report, it will damage your credit score as well as how you appear in the eyes of a potential lender.

If your debt is listed as charged off instead of discharged, you'll want to dispute this information.

Particularly common after Chapter 13 bankruptcy, former creditors will sometimes report that you still owe them money even after your debt has been discharged. Secured creditors are most guilty of this.

For example, let's say that you had a car that you were upside down on that you surrendered to the bank. Let's say that you owed $40,000 and it was only worth $30,000.

That $10,000 is no longer secured debt-- it turns into unsecured debt. This debt either gets paid or doesn't get paid in accordance with the Chapter 13 plan that resulted from the court proceedings. If the debt is discharged, the money is not owed to the lender.

If you believe that you don't owe a creditor more money but they are still reporting that you do on your credit report, you'll want to dispute this information with the creditor, the credit bureaus that are reporting the incorrect information, or both.

In bankruptcy cases, sometimes debts will be reaffirmed rather than discharged. This occurs when a debtor wants to pay a specific debt even though it could potentially be discharged through the bankruptcy process.

For example, a debtor might choose that they want to hold on to their car and continue paying the debt on it. This debt could then be reaffirmed rather than discharged. The debtor is, therefore, still responsible for paying back the money they owe.

Sometimes, this will show up on a credit report as discharged in bankruptcy rather than reaffirmed. You can correct this information on your credit report by disputing it with the credit bureaus or the creditors themselves.

When a married couple has joint debts and one spouse files for bankruptcy while the other does not, the non-filing spouse will likely see information on those joint accounts that say something along the lines of "included in bankruptcy." This is to be expected.

However, sometimes the non-filing spouse will actually see information on their credit report that claims that they themselves filed for bankruptcy either under the public records section or attached to one of their solely-owned accounts.

Incorrect information like this on your spouse's credit report can be very damaging to their score unnecessarily. You'll want to dispute the information in order to have it corrected.

Bankruptcy can, in some ways, be a fresh start, but you don't necessarily get to begin with a completely clean slate. Discharged debts will show up on your credit report and remain there for some time, and bankruptcy will show up in your public records.

Even if you aren't able to completely remove discharged debts from your credit report, there are a number of things you can do to rebuild your credit over time. Though it can feel like an uphill battle, it's worth investing in your credit to ensure that as many financial opportunities as possible are open to you down the road.

Are you searching for more resources to help you build your credit? If so, make sure you check out our Credit Building Tips blog.

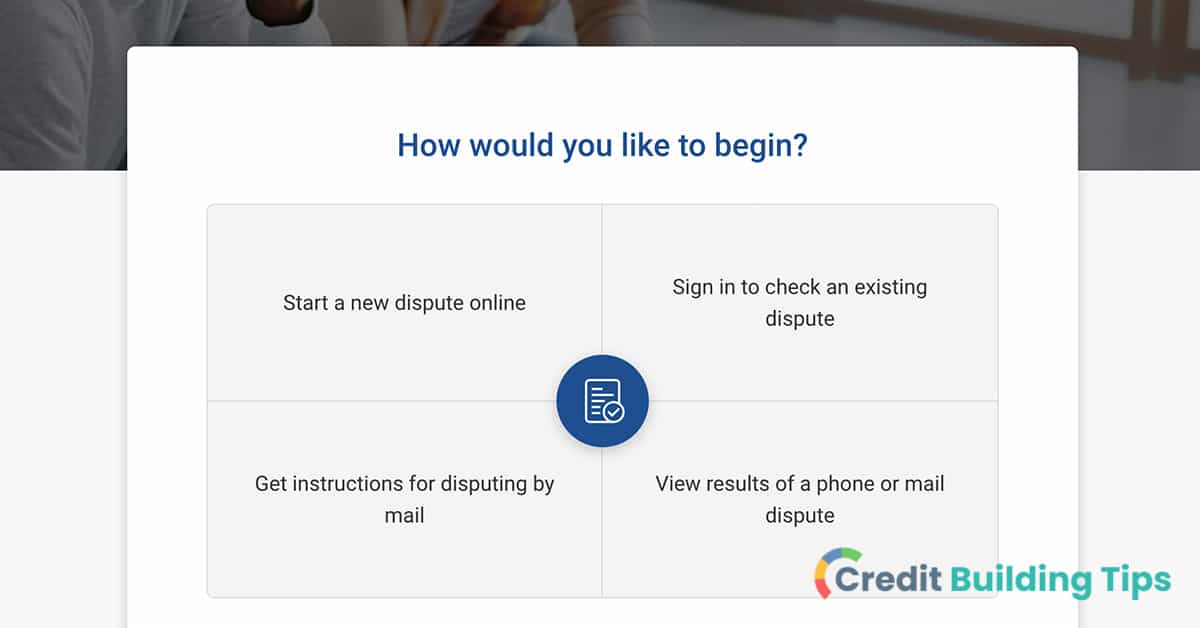

When incorrect information shows up on your credit report, the next step is to open a dispute with the credit bureau that is displaying the error. This opens an investigation, which normally takes about thirty days.

During this time, the account in question will likely show a "dispute comment." This is an indication that there is currently a dispute under investigation.

Dispute comments usually shouldn't be a problem, but sometimes mortgage lenders will want them removed because they will temporarily mask the account from being calculated as a part of your credit score. Additionally, you might want a dispute comment removed because it is making your credit score artificially low.Removing dispute comments isn't always a good idea, so it's important to determine whether or not it will be advantageous to you. You can ask credit bureaus to remove dispute comments by calling them and talking to a representative or sending a letter via mail or fax.

Anytime you file a dispute regarding one of the accounts that appear on your credit report, an investigation into the claim will begin. This is the case whether you question the validity of an account or information about an account with the credit bureaus or with a debt collector.

These investigations usually take about thirty days to be completed. During this time, the account will be marked on your credit report as “disputed.”

Your right to dispute information on your credit report is outlined in the Fair Credit Reporting Act (FCRA). In this Act, companies that provide information to credit bureaus have:

“...specific legal obligations, including the duty to investigate disputed information.”

Since there will be a period of time after you file a dispute and before the investigation is over, this comment serves to indicate that there is a dispute or disagreement regarding specific information that is found on your credit report. In most cases, dispute comments are added when a consumer believes that certain information is incomplete, inaccurate, or misrepresented.

If you are looking at your credit report and you see a dispute comment, there are two primary forms it can take:

This first type of dispute comment means that there is an active investigation underway after a dispute has been filed. When applying for a home loan, lenders will usually want to see these notes removed before determining whether to approve you for a mortgage and, if so, what rates and terms to offer. This is because the account won’t be factored into your credit score via FICO credit scoring models.

If the second type of dispute comment appears, it means that a resolution has been reached after the completion of the investigation. This particular type of dispute comment won’t be something that bothers lenders, as the account will once again be incorporated into your credit score calculation.

Are you ready to improve your credit score and clean up your credit report? Check out our guides to credit repair hacks, credit repair services, and repairing your credit after you're the victim identity theft.

Removing a dispute comment isn’t always necessary and isn’t always favorable. In the next section, we’ll discuss when you should and should not ask for dispute comments to be removed from your credit report. In this section, however, we’ll look at the steps you need to take to have a dispute comment removed, assuming that you have already decided that this is the right course of action.

The fastest way to have dispute comments removed from your credit report is going to be calling the credit bureaus. Though this can be frustrating as it often means sitting on hold for a while, you’ll find that it’s a much quicker way of going about it than sending a letter through the mail.

Here are the numbers and subsequent menu items to select that you’ll want to try in an effort to speak with an actual human:

If these numbers don’t work, your next best bet will be pulling your free credit report from AnnualCreditReport.com, which is a site authorized by Federal Law and put together by the three main credit bureaus. On each of your credit reports, you should be able to find a phone number that you can call in addition to a personal credit report ID number.

Once you have someone on the phone, you’ll want to tell them that you want to have a dispute comment removed from some of your accounts. If you are doing so because you are pending mortgage approval, mention that the lender has asked you to do so in order to move forward with your home loan.

If you’d prefer to write the credit bureaus rather than call them, you will want to enclose a copy of each of the following with a letter sent via certified mail or fax:

Here are the addresses you can use to mail your request to have a dispute comment removed:

The fax numbers for each credit bureau are not listed on their website, which means you might need to call and confirm the current and correct fax number to use. Given this, you might find that simply dealing with deleting the dispute comment over the phone is the quickest way to resolve the issue.

You might think that it’s always a good idea to remove dispute comments from your credit report, but this isn’t necessarily the case.

There are really only two reasons that you should go through the trouble of asking the credit bureaus to remove dispute wording from your credit report:

If you have derogatory marks on your credit report, it can really make it difficult to get approved for a loan with good rates and terms. If it's time to clean up your credit report, take a look at our guides to removing charge offs, removing collections, removing hard inquiries, removing evictions, and removing 30-day late payments from your credit report.

It isn’t always easy to know whether or not removing dispute comments will increase your credit scores. However, if you know that the account is in excellent standing, you might want to remove the dispute comment if you are currently applying for a loan or line of credit.

That being said, it’s possible that the account is increasing your score in one way and decreasing your score in another, leaving you with a net neutral result when removing the dispute comment. It can be pretty tricky to figure out whether an account is going to help or hurt your score, so you’ll want to proceed with caution.

If you’re applying for a home loan, there’s a chance that your mortgage program might require that dispute comments are removed before the process can be completed.

The four most common mortgage programs out there are:

Each of these programs is going to have its own unique underwriting rules. The underwriting rules for each respective program are going to govern things like:

In many cases, mortgage loan programs will allow some types of dispute comments to remain on a credit report. For example, FHA loans don’t require that dispute comments are removed from medical accounts and accounts with zero balances. Additionally, dispute comments don’t have to be removed for an FHA loan if the total balance of these accounts in dispute is less than $1000.

When the digital version of your credit report is run through the automated underwriting service run by your loan program, it’s possible that dispute comments won’t trigger an alert regarding a disputed account.

In some cases, you might find that it is a better option to switch loan programs rather than to remove dispute wording on your credit report. Once the account is unmasked, it's possible that it will drop your credit score enough that you will no longer qualify for the loan program you were initially approved for.

Before we sign off, let's take a closer look at the answers to some commonly asked questions about credit report dispute comments.

Credit report disputes can indirectly impact your credit score. FICO credit scoring systems will not take accounts that are actively in dispute into consideration when calculating your score. Even though the dispute comment will show up on your report, the entire account will not be used to help determine your score.

Depending on the status of the account, this could mean that your credit score is artificially lower or higher than it would be if the account was factored in. Until the comment is removed, FICO credit scoring models will not incorporate the account into their calculations.

If you are applying for a home loan, a lender will often be able to see that there is a dispute comment on your report and will know that this is impacting your true credit score. They will, therefore, likely want the comment to be removed before making a decision about your loan so that they know they are viewing an accurate credit score.

Dispute comments will usually stay on your credit report until the investigation has been completed and the dispute has been resolved. At the point that the dispute is resolved, the information on your credit report will be updated accordingly if necessary.

That being said, sometimes a credit report will indicate in a comment that there had been a dispute in the past and the dispute has been resolved. In this case, these comments won't mask the account for the purposes of calculating your FICO score.

How long it takes to remove a dispute comment from your credit report is going to vary. If you are able to talk to a representative from the credit bureaus on the phone, you might find that the dispute comment has been removed in as little as four business days. If you choose to contact the credit bureaus via fax or snail mail, it might take as long as thirty days.

Anytime you find inaccurate information on your credit report, you can dispute it with the credit bureau. All of the credit bureaus have online portals that you can use to dispute information, making the process simple and easy to get started.

It's worth noting that there are certain items on your credit report that aren't disputable. Though it is within your legal rights to dispute credit report information, some info is maintained "as a matter of factual record." Though it is possible under some circumstances, you usually cannot remove information that is factually correct.

The outcome of a dispute could impact your credit, but the dispute itself should have no effect on your credit.

For example, let's say a late payment showed up on your credit report, but you did actually pay on time. If you dispute the information and it is corrected, it will probably help your credit score.

If you are disputing personal information such as the name or address that appears, though, this won't impact your credit score.

The nature of the information that is being disputed will impact the results of the dispute. Once the dispute has been resolved, an outcome description might be added to your credit report.

If you are filing a dispute that is related to your personal information, it can result in:

If you are filing a dispute that is related to accounts, inquiries, or bankruptcy, it can result in the following:

Improving and building your credit might not sound like your idea of a good time, but you might get a bit more excited about it when you realize how much money it could save you and the financial opportunities it can open up for you.

Cleaning up your credit report and boosting your credit score can end up saving you tens of thousands of dollars in interest over your lifetime, as you'll end up receiving much more favorable rates and terms when you borrow money.

Beyond that, credit scores and reports can be taken into account when you apply for an apartment, a job, or insurance. When you consider just how impactful your credit is on the practical realities of your life, it's worth taking the time and putting in the effort to improve your credit.

Are you ready to begin the journey of cleaning up your credit report and boosting your credit score? Make sure you take a look at all of the resources on our Credit Building Tips blog.

Have you ever wondered how merchants can ensure that a credit card being used during a transaction isn't being used fraudulently? When someone enters a credit card number online or reads it over the phone, after all, the merchant has no way of knowing whether the consumer actually physically has the card in their posession.

This is where a CID number comes in-- also known as a CVV2 or CVC2.

CID on a credit card stands for "card identification number." It is a three or four-digit number that can be found on the card that serves to add additional security for online or over-the-phone transactions.Let's take a look at everything you need to know about CID numbers.

CID stands for "card identification number." A CID number is a security feature that is used when you are making a transaction when your card isn't physically present. This is a three or four-digit number that can be found on your credit card.

You also might hear the terms:

All of these terms of usually used interchangeably.

This three or four-digit number essentially offers a payment system a method to determine whether your card is authentic.

There are two things that a CID number helps to verify:

These verification numbers aren't contained in the magnetic stripe information of the card. Instead, they are only on the card itself.

Additionally, these numbers can't be found on credit card statements or on receipts. Using a CID helps payment processors ensure that they aren't accepting counterfeit cards.

You can find the CID number on a Visa, MasterCard, or Discover card on the back of the card. It will be located to the right of the credit card number near the signature area. CID numbers on these types of cards consist of three digits.

On American Express cards, the CID number is actually located on the front of the card. It will appear above the account number on the card's face. It usually is on the right side, but it will sometimes appear on the left side of the card.

Many people don't realize exactly what function the security code on their card offers. They sometimes give it out when they don't need to because they think it is necessary information, even in in-person transactions. Stick with us as we answer some of the most common questions about CID to help ensure your credit card info stays safe and secure.

You should never need to give your CID to another person when you are making a sales transaction in person.

In fact, most online retailers will require that you enter your CID when you are making purchases in an effort to prevent fraudulent transactions. That being said, you always want to make sure that you only give your credit card information to reputable companies.

For this reason, it's important to always be careful when entering your card information online.

Here are some steps you can take to protect your financial information online:

Did you overdraw your bank account and you're worried it's going to ding your credit? Check out this article to learn more about whether a bank overdraft affects your credit score.

You will end up with a new CID code when you get a new credit card. This is the case whether you apply for an entirely new card or if an old card expires and you need to replace your existing card.

When you use a credit or debit card in person, you can supply a signature, pin, ID, or another type of verification when making a purchase. However, if you're making an online purchase or buying something over the phone, the merchant and the card processor have no way of knowing for sure that you are actually in possession of the card. You could, instead, be someone who has the name and card number of someone else.

People can steal credit card numbers through a number of venues, including:

Though a CID number isn't a completely foolproof security measure-- after all, not all merchants ask for it-- it does serve as an extra layer of security against fraudulent activity.

Was your identity stolen and it took a serious toll on your credit file? This guide goes over how to repair your credit after ID theft and fraud.

Yes, a CVV, CVC, CVV2, and CVC2 are all acronyms used to describe the same security code on your credit card.

If someone has your CID without any of your other credit card information, they probably won't be able to do any damage. However, if they have your credit card number, your name, your CID, and other important info, you could become a victim of credit card fraud.

If you find yourself in this situation, follow these steps:

Are you trying to improve your credit health? Check out these posts about removing charge-offs, collections accounts, hard inquiries, evictions, and 30-day late payments from your credit report.

Credit cards allow us a tremendous amount of freedom by letting us buy things now and pay for them later. This freedom also comes with responsibility-- the responsibility to both use credit responsibly and keep our credit card information secure so it doesn't fall into the hands of identity thieves.

In order to make sure that your credit card accounts are safe, you'll want to practice the following:

Building a healthy credit score and maintaining it can seem like a big chore sometimes. After all, there are many different moving parts that go into keeping a credit score and credit report in good shape.

Your CID is one of the things that protect you from credit card fraud and therefore protects your credit report. After all, if an identity thief uses your credit card information to make purchases online or over the phone, it can end up resulting in marks on your credit report when payments aren't made on time.

Even though maintaining good credit health can feel like a lot of work, it's well worth the trouble. Having great credit can make it much easier to borrow money when you need to, as well as ensure that you get the best rates and terms when you do. Over your lifetime, having a healthy credit score versus a poor credit score can save you thousands and thousands of dollars.

Are you on a mission to improve your credit? If so, head over to our credit building blog to learn more tips and tricks for boosting your credit score and fixing your credit report.

If your credit score has seen better days, you might be struggling to get a loan, rent an apartment, or qualify for a credit card.

To help improve your chances as an applicant, credit repair services will often promise to help boost your credit score. These are companies that will review your credit reports and act on your behalf to address any negative items with the credit bureau.

Credit repair services will help you dispute incorrect information on your credit report in exchange for a fee-- usually a monthly fee ranging from $20 to $150. There can be additional charges for these services, including start-up fees and cancellation fees.It's important to understand that there are scammers out there masquerading as credit repair services, so you'll want to learn about the red flags to watch out for. Additionally, it's worth noting that credit repair services don't have magical abilities to clean up your credit report-- everything they do is something you can do for yourself for free.

Credit repair services help you come up with a plan you can use to repair your credit and will act on your behalf in order to dispute inaccurate information.

Essentially, these companies can help you remove errors or other incorrect marks on your credit report that are damaging your score. What they can't do, however, is remove accurate information.

Some of the types of items that a credit repair service can remove include:

You'll often find that credit repair companies will offer extra features for additional fees, such as:

In many cases, these extra services aren't worth the steep fees that are charged.

If your credit is less than ideal and you want to improve your score, the concept of credit repair services might sound too good to be true.

The truth is, though, that a credit repair company isn't going to be able to help you remove accurate information from your credit report.

For instance, if you have a high credit utilization ratio, several late payments, or other derogatory marks, credit repair services won't be able to help if the information is correct.

Did you overdraw your bank account and you're worried it's going to ding your credit? Check out this article to learn more about whether a bank overdraft affects your credit score.

When shopping around for credit repair companies, you'll find that they all tend to have their own pricing structure. Typically, though, they sell packages of services and charge fees monthly.

In addition to the monthly fee, some companies charge enrollment or set-up fees as well as fees when you cancel the service. You can find some companies that will offer a money-back guarantee, but this isn't always the case.

It's common for companies to have policies that essentially require you to stay signed up for several months.

For example:

Only you can decide whether or not it's worth the cost to hire a credit repair company, but it's important to note that pretty much anything a credit repair service can do for you, you can do for yourself.

To do so, you'll want to follow these steps:

Was your identity stolen and it took a serious toll on your credit file? This guide goes over how to repair your credit after ID theft and fraud.

The idea of paying someone to repair your credit report can seem a bit too good to be true at first, and there are certainly companies out there that make promises they simply won't be able to keep. Here are some of the most commonly asked questions about credit repair companies to help you determine whether paying for one of these services is the right choice for you.

It can take several months to start seeing results after you've signed up for a credit repair service. The length of time it takes for your credit to be fully repaired can be six months or even longer.

It's also possible that the inaccuracies you had fixed will end up showing up on your credit report again down the road, so you'll still want to keep an eye on your report.

You can find credit repair companies that operate nationally, while others only offer their services in certain states.

Depending on the package of services you purchase from a credit repair company, you also might receive credit monitoring services. This means that they will keep an eye on your credit report for any changes that could potentially stem from fraudulent activity.

Are you trying to improve your credit health? Check out these posts about removing charge-offs, collections accounts, hard inquiries, evictions, and 30-day late payments from your credit report.

Unfortunately, scammers can be attracted to the field of credit repair. There are plenty of legitimate companies out there, but you'll want to be on your toes when choosing one to make sure you aren't sending money to a party that has no interest in helping you.

There are a number of things you'll want to watch out for when seeking credit repair services.

According to the Consumer Financial Protection Bureau, some of the signs of a credit repair scam include:

It's important to understand that pretty much anything a credit repair company can do for you is going to be something you can do for yourself. They don't have magical abilities to fix your credit report, but they do have experience going through the dispute process and otherwise engaging with the credit bureaus.

Additionally, there is still some work you will have to do on your own, even if you hire credit repair services.

All that being said, some consumers find that it is worth the money to have credit repair companies take on some of the work of disputing inaccurate information on their credit reports.

While credit repair and credit counseling services might sound kind of similar, they are actually two very different services.

Credit counseling is tailored to your specific situation and consists of receiving financial advice from a credit counselor. They will also be able to offer you resources that give you the information you need to improve your financial situation. Consumers will typically seek credit counseling when they need advice on how to get themselves out of debt.

Your credit profile will not be wiped clean by a credit repair company. Legitimate negative information on your reports, such as bankruptcy, default, or late payments, will age off your reports after a certain number of years, depending on the nature of the mark.

Here is how long it takes for specific information to fall off of your report:

Credit repair services are only able to dispute incorrect information on your credit report. Some services might offer to send a goodwill letter to your creditor or debt collector on your behalf in order to ask them to remove the derogatory marks. However, creditors and debt collectors are not obligated to honor these requests.

Unfortunately, we can't just wipe the slate clean and start over with our credit reports. What we can do, though, is take actions that help to improve our credit scores.

Some of the things you can do to rebuild your credit include:

Believe it or not, it can actually hurt your score to open a new credit score-- at least immediately. It will, eventually, start to help your credit score.

This is because the credit card company will run a hard pull of your credit when you apply, which can ding your credit.

However, you'll soon start to appreciate the benefits of having a new card because your credit utilization ratio will drop, which is a metric where lower is always better. Making up roughly 30% of your FICO score, giving yourself a more advantageous credit utilization ratio can be a fairly quick way to boost your credit score.

Whether or not it's worth the cost to hire a credit repair service is something that only you can decide. It's important to be diligent when choosing a credit repair service, though, as there are definitely scammers out there that make lofty promises and don't return any results.

Beyond that, remember that credit repair companies cannot delete correct information from your credit report. They can only dispute incorrect information with the credit bureaus on your behalf. In some cases, they might also send goodwill letters to debt collectors on your behalf to attempt to have accurate negative accounts removed, but there is no guarantee that this effort will be successful.

If you don't want to take the time or deal with the headache of interacting with the credit bureaus when there's an error on your report, you might find that it's worth it to pay a credit repair company. That being said, you might find that the money is better spent going toward your debt and that you can actually handle the disputes on your own without paying start-up fees, monthly fees, and cancellation fees.

Are you ready to improve your credit score and make yourself a more appealing borrower to lenders? Make sure you check out our credit building tips blog for more resources to help you boost your credit and clean up your report.

Having a less-than-ideal credit score can have some very impactful real-life consequences. It can mean it's more difficult to be approved for a mortgage or car loan, you'll pay higher interest rates when you do borrow money, and it can ultimately affect your ability to begin building wealth.

Beyond that, a bad credit score and a credit file filled with derogatory marks can even make it difficult to rent an apartment, it can increase your insurance premiums, and it might affect your career opportunities.

If your credit score has seen better days, there are a number of credit repair hacks you can use to help increase your score and improve your credit profile. The important thing is to understand which elements are hurting your credit score the most so that you can start addressing the factors that are most adversely impacting your score right away.Without further ado, let's jump in to help you determine the best actions you can take to improve your credit.

One of the most important things you can do to ensure that your credit score is where you want it to be is to check your credit report regularly.

There are three major credit reporting agencies-- Experian, Equifax, and TransUnion. At each bureau, you have a credit report.

It's worth checking all three credit reports because not all creditors report to all three credit bureaus.

You can receive a free credit report from all three agencies through the Federally authorized site AnnualCreditReport.com.

Your credit score is calculated using your credit report. You can find out what your credit score is through a soft inquiry using one of the major credit scoring websites. Some credit card issuers also provide credit score tools.

The Federal Trade Commission reports that 25% of people have had errors on their credit reports. You, therefore, shouldn't assume that errors and inaccurate information are in any way rare, and you should always keep an eye out for accounts or other info that isn't correct.

If you do find any errors on your credit report, you'll want to remove them right away. You can dispute errors on your credit report at all three bureaus. The easiest way to do so is by using their online platforms for disputing credit report errors.

Sometimes, there's negative information on your credit report that is accurate. Whether it's a collections account, missed payment marks, or another derogatory mark, it isn't always possible to remove negative information from your credit report. However, since this type of info can be detrimental to your credit, it's always worth giving it a shot.

Has a creditor written off your debt? Learn how to remove charge offs from your credit report in this guide.

If you have a missed payment on your credit report, you can ask your creditor for a goodwill adjustment. They aren't obligated to remove correct information from your report and will sometimes argue that they are bound to report accurate info to the credit bureaus.

Is your credit damaged because your identity was stolen? Check out our post on how to repair your credit after identity theft and fraud.

Having a collections account on your credit report can have a negative impact on your credit score. If a past debt of yours has been sent to collections, you can try and negotiate with the collections agency through what is known as a pay-for-delete agreement.

Make sure you receive their end of the bargain in writing before making a payment if you do strike a deal with them.

Your payment history is the most important component of your credit score when calculated using either of the two most popular credit scoring models-- FICO and VantageScore. In a FICO credit score, your payment history accounts for 35% of your score, and it makes up about 40% of your score in a VantageScore credit score.

Of course, never missing a payment is easier said than done. However, there are a few steps you can take to ensure that you get a derogatory mark for missed payments and to help keep your credit score as high as possible.

There are few things as frustrating as missing a bill payment simply because it slipped your mind. One of the best things you can do for your credit is to set up automatic payments. This way, you can remove human error as a factor when it comes to making payments on time.

If you do realize that you had a bill due recently and you didn't have automatic payments set up, don't panic.

If possible, make any missed payments before thirty days have gone by to ensure that it doesn't decrease your credit score.

If you missed a payment and have been charged a fee, consider calling your creditor and asking them to waive the fee.

While this fee doesn't impact your credit score, you want to make sure that you aren't paying any money unnecessarily that could otherwise be going toward paying down your debt.

Your credit utilization ratio accounts for 30% of your FICO Score calculation and 20% of your Vantage Score calculation.

When it comes to credit utilization ratios, lower is always better. Experts advise that you work to keep your credit utilization ratio below 30%.

There are a number of things you can do to make sure your credit utilization ratio is as low as possible, including paying down your debt, increasing your credit limit, timing your payments, reducing spending, and more.

Paying down your debts will mean that you are using less of the credit that has been extended to you, reducing your credit utilization ratio.

Your credit utilization is a ratio that represents the percentage of your credit limit that you're using.

If you want to increase your credit score quickly, paying down debt (and not taking on new debt) can help your score improve dramatically.

Paying off high-balance cards is one of the fastest ways to lower your credit utilization ratio.

Beyond your overall credit utilization ratio, there is also something known as a line-item utilization ratio.

For this reason, it can make sense to pay down high-balance cards first.

Another important factor when it comes to your credit utilization is the number of accounts you own that have balances. Your score will benefit from having fewer accounts with balances.

If you want to boost your credit score, consider paying down your low-balance accounts to reduce the total number of accounts that are carrying a balance.

Another way to ensure that you aren't carrying a balance on too many accounts is to consolidate your debt.

Beyond that, debt consolidation can help you pay off your debt more quickly when you snag a lower interest rate. It can also be much simpler to manage debt when you are only making one payment instead of many.

Important note: While debt consolidation can be a powerful tool to reduce debt and increase your credit score, you have to use it carefully. If you end up running up debt on your original cards again in addition to the balance transfer card debt, you can find yourself in a deeper hole than you initially started in.

Lowering your interest rates on your existing credit cards won't directly impact your credit score. However, the less interest you pay on each card every month, the faster you will be able to pay down your debt.

The worst that could happen is they say no. If they do say yes, it could save you hundreds or thousands of dollars in interest.

One of the fastest and easiest ways to boost your credit score is to increase your credit card limits. That being said, there are a few things you'll want to consider before you ask your issuers to increase your limit.

Since your credit utilization ratio is a number that relates how much credit you have available to the debt you owe, increasing your credit limit can lower your credit utilization ratio quickly and easily in a way that improves your credit score.

Once you've paid off old cards, it's best not to close the accounts in most cases.

In some cases, though, it might make sense to close old cards.

For example:

Additionally, if you have really struggled with overspending, you might find it is worth closing old accounts so that you aren't tempted to rack up more debt.

It's reasonable to assume that by simply paying off your cards each month, your credit utilization ratio should stay low. However, it's also important to consider when creditors are reporting to credit bureaus.

Creditors and lenders will run a hard inquiry every time you apply for credit or a loan.

Additionally, new card accounts can lower the average age of your accounts, which can also negatively impact your score.

Another way you can build credit is through a method called credit piggybacking. The most common way to improve your credit by associating yourself with someone else's credit is to become an authorized user, but you can also open a joint account or find a co-signer for a loan.

One of the fastest ways to build credit is to become an authorized user on a seasoned tradeline.

When you become an authorized user on someone else's account, it can quickly add years of credit history to your report.

Though there aren't many issuers that offer joint credit cards anymore, it's possible that you can benefit from your partners' good credit by opening a joint account.

If you need to take out a loan but you have less than ideal credit (or very little credit history,) finding a co-signer can be a very useful tool. Though it can be difficult to find someone to take on this role, a co-signer can help a primary borrower build credit over time so long as they make on-time payments.

If you have no credit or a very limited credit history, it can be difficult to know how to start building credit. In these instances, a credit builder loan can help individuals build credit and boost their scores when they make regular, on-time payments.

If you are what is known as "credit invisible"-- i.e., you don't have a credit score-- this is a method you can use to gain additional access to financial services and products.

Another loan you can use to help rebuild credit after it's been damaged is an installment loan. I've personally used this type of loan to improve my credit.

If you are going to shop around for a loan or a new credit card soon, you'll want to be thoughtful about adding additional hard inquiries to your credit report.

While each hard inquiry usually only takes a few points off your credit score, too many of these on your report can be a red flag to lenders.

For mortgages, auto loans, and student loans, inquiries that occur during a fourteen day window are considered one single inquiry. This is because it is understood that savvy consumers will shop around for the best rates and terms when borrowing money.

It's worth noting that FICO scores don't group together inquiries for credit cards-- each one shows up as its own separate hard pull. With the VantageScore model, however, inquiries made during a fourteen-day period are grouped together for any type of account.

If you've used some of these tips and tricks to improve your credit, it still can take some time to see the fruits of your labor show up in your credit score.

Only mortgage lenders can provide rapid rescores. If you aren't planning on applying for a home loan, this means that updating your credit report quickly will require that you manually contact each of your creditors after you've corrected errors, paid down your balances, and otherwise improved your credit profile.

When you contact your creditors, you can ask them to send a verification letter that reflects the new information on your account. This letter can then be forwarded to the credit bureau so your information will be updated.

The word "triage" is:

When you want to increase your credit score quickly, you'll want to use a similar approach. You should take a look at your credit report and find out which elements are most adversely affecting your score. You can then work to deal with these issues first before moving on to less urgent, less impactful aspects of your credit profile.

Finally, one of the most important things you can do for your credit score and your overall financial health in the long term is to ensure that you always use credit responsibly.

However, irresponsibly using credit cards can mean that you rack up more debt than you can afford, significantly damage your credit score, leave you with high-interest payments, have accounts go into collections, and so on.

No one likes spending their free time trying to improve their credit score, but it's a project well worth dedicating some time to. This is particularly true if you are expecting to apply for a loan or credit card in the near future.

There are a lot of things you can do to improve your credit, but not all actions you take in this regard are created equal. It's, therefore, a good idea to make sure you understand which elements of your credit report are most damaging so that you can focus on pursuing the most impactful factors first.

If you're motivated to improve your credit score and clean up your credit report, make sure you check out our credit-building tips blog for more useful resources!

According to the 2022 Identity Fraud Study conducted by Javelin Strategy & Reserve, 15 million consumers in the U.S. were victims of identity theft.

Identity theft isn't just scary and potentially expensive, but it can also wreak havoc on your credit for years to come if you aren't careful.

Repairing your credit after identity theft can be a time-consuming process, but it's worth it to ensure that you don't suffer the consequences of bad credit down the road. You'll need to communicate with any creditors and companies where fraud occurred, dispute incorrect information on your credit reports, freeze your credit, and more to make sure that your credit isn't damaged by the experience.As with most things, prevention is the best cure to identity theft when it comes to your finances and your credit. However, the next best thing is to regularly monitor your credit reports, credit card statements, and bank statements so you can catch strange or unusual activity right away.

When someone uses your personal information without your permission, it's known as identity theft.

An individual can use your personal information to commit identity theft in a number of different ways, including:

Obviously, any of these occurrences is a huge problem in their own right. When you add in the fact that it can have an impact on your credit reports and credit scores, it only adds insult to injury.

Before we get into how to repair your credit after someone has stolen your identity, there are a few steps you're going to want to take to ensure that the fraudster isn't able to do any further damage.

There are essentially three different categories of actions you will want to take when someone has stolen your identity. These are:

This doesn't necessarily mean that you will want to go through these three stages in order, though. When you realize that your identity is stolen, you will essentially need to perform a number of important actions as quickly as possible to ensure that no further damage is done and that your personal and financial information is protected.

Here is a breakdown of the steps you'll want to take after you realize that your identity has been used for fraudulent purposes:

In the next section, we will take a closer look at the steps that involve repairing your credit after identity theft and fraud.

Now that you have seen a full list of the steps you will want to take after you realize that your identity was stolen let's take a closer look at the actions you'll need to take in order to repair your credit.

Different credit scoring models vary slightly in how they weigh factors, but in general, they place a similar amount of importance on each type of information. The primary factors credit scores take into account(presented in order of importance) are:

If hard inquiries are impacting your credit score, this guide looks at how to remove hard inquiries from your credit report.

If an identity thief steals your credit card information or opens fraudulent loans or cards, missed payments might be accruing. This could be happening on cards you opened yourself or accounts you don't even know about.

The good news is that your liability is limited for paying back fraudulent purchases so long as you catch it quickly and report it right away, thanks to Federal law. The bad news is that your credit reports will show missed payments that have a negative impact on your score and how you appear to potential lenders as a borrower.

Even if you file these disputes immediately after the fraud occurs, it can still take some time for the changes to reflect on your credit report and in your scores.

If an identity thief racks up debt in your name, it will have a negative impact on your credit utilization rate. Experts typically recommend that you keep your credit utilization rate at 30% or under. Lower is always better.

Once the problem has been remedied, your credit utilization rate will return to its normal level.

Though identity thieves likely won't have a direct impact on the length of your credit history, they can open new cards and get new loans that will wreak havoc on your credit score.

You will need to report the fraudulent activity to any lenders or creditors that allowed the thief to borrow money in your name and close the accounts. It can take time for the fraudulent accounts to be removed.

Identity theft shouldn't have an impact on your credit mix, as it is unlikely that a fraudster will close your legitimate accounts. This is one of the few factors that you don't have to worry about, but, unfortunately, it is also one of the least impactful factors on your scores.

If an identity thief has taken out a loan or opened a credit card in your name, it means that hard inquiries were made into your credit report.

Hard inquiries will remain on your credit reports even once you have closed fraudulent accounts and removed them from your credit report. You will need to dispute hard inquiries with the credit bureaus to ensure they don't impact your credit or your ability to borrow money in the future.

You will want to take action quickly when you realize that your identity might have been stolen.

Here are the steps you'll need to take:

On a mission to fix your credit? Take a look at our guides to removing a 30-day late payment, deleting a collection in exchange for payment, and removing derogatory marks on your credit report.

If you suspect identity theft, take a look at both your credit card and bank statements.

On credit card statements, look for any unfamiliar charges. You don't want to ignore charges just because the amount is small-- many scammers will start with small charges to see if it works before making more expensive purchases.

Even if you don't suspect fraudulent activity, it's important to review your credit card statements regularly.

On your bank statements, keep an eye out for strange activity and contact your bank if there are any unusual charges you don't recognize.

AnnualCreditReport.com is the site authorized by Federal law where you can request a free credit report from all three of the major credit bureaus.

Did your credit score drop unexpectedly? Take a look at this post about why your credit score might have dropped by 100 points or more.

Now that you have your credit report in hand, here is what you will want to look for:

It's best to follow up on any strange activity or marks on your credit report, even if it doesn't seem like a big deal or isn't currently impacting your credit score. If someone has your personal information, there's a good chance they will continue to do further damage.

You'll also want to check public records for civil court judgments or liens in your name. An identity thief that stole your ID could be masquerading as you in a way that impacts your public record. Since civil court judgments and liens no longer appear on your credit report, you'll want to contact the recorder's office in your county to look at your public records.

There are a number of steps you'll need to take if there has been fraudulent activity in your name. Some of these were briefly touched upon in the section "What to Do If You've Been a Victim of Identity Theft."

First, you'll want to call any companies where the fraud has occurred. To stop further damage, ask credit card companies and lenders to close or freeze any and all fraudulent accounts.

You'll also want to ask for a letter confirming that:

Beyond placing a fraud alert with all three credit bureaus, you'll also want to dispute any incorrect info that can be found on your credit report. All three credit bureaus-- TransUnion, Equifax, and Experian-- have online pages where you can begin the dispute process.

You'll also want to tell them to stop reporting the debt to credit bureaus and ask them for more details about the debt.

Now that you've been through the process of dealing with identity theft, you're likely motivated to avoid this experience in the future. Once you have worked everything out with the credit card companies, lenders, credit bureaus, debt collectors, and any other involved parties, you'll want to make sure that you take any and all necessary steps to ensure your identity and credit are protected in the future.

For more info about how to protect yourself from ID theft, scroll down to the section entitled "How Can I Protect Myself From Identity Theft?"

There are a number of things you will want to always keep an eye out for when it comes to identity theft and fraud.

Some of the signs of identity theft can include:

Before we sign off, let's touch upon some other frequently asked questions about identity theft and credit.

There are a number of different ways that identity thieves can steal personal information from individuals.

These include:

Do you need to repair your credit report so you are better able to qualify for a mortgage or another loan? Make sure you check out our articles about removing collections from your credit report, removing hard inquiries from your credit report, and removing evictions from your credit report.

The thought of someone coming into possession of your personal information is truly terrifying. Luckily, there are a number of things you can do to prevent identity theft from occurring.

Here are some habits you can practice in order to avoid your private information ending up in the wrong hands:

Having your identity stolen can be an overwhelming and terrifying experience. With your personal or financial information, thieves have the ability to rack up debt, take out loans, or even masquerade as you in police interactions.

Are you on a mission to rebuild your credit and make sure that you always have the ability to borrow money and take out loans with the best terms? If so, make sure you check out our credit building blog.

If a borrower misses several months of payments, the creditor might give up on trying to collect the debt and write it off as a loss. When this happens, the account is designated as a charged-off account or simply a "charge-off."

Just because the creditor has charged off the account doesn't mean that you aren't still expected to pay back the debt, though. They might sell your debt to a third-party collections agency, which can also appear as an account in collections on your credit report.

A charge-off on your credit report will typically remain there for seven years starting from the date that you first missed a payment. You can remove inaccurate charge-off accounts by disputing them with the credit bureaus. You can attempt to have accurate charge-offs removed by negotiating with the creditor or debt collector.Let's take a closer look at everything you need to know about charge-offs and what you can do to remove them from your credit report.

When you take out a loan or a line of credit, the creditor or lender is expecting that you will pay back the money that you owe based on the agreement you’ve made. However, if you are unable to keep up with your payments or completely stop paying toward your loan, it can mean your account becomes delinquent.

After a certain number of days, the creditor might choose to charge off your account. In many cases, the length of time after an account is delinquent before a creditor charges it off ranges between 120 and 180 days.

Charge-off is the term used when a creditor has closed your account to future changes and written it off as a loss.

When your account is charged-off, it means that the creditor has given up on collecting the debt from you and written it off as a loss. This doesn’t mean that you’re off the hook, though.

With your debt now in the debt collection agency's hands, the debt collector will try and get you to pay off the debt. They can send you letters, call you, email you, or text you in an attempt to collect the debt. They can even file a civil lawsuit against you in order to recoup the money that is owed.

When an account is charged off, it doesn't mean that you are no longer obligated to repay the debt.

Yes, charge-offs will appear on your account history along with other negative information, such as missed or late payments. Negative information typically stays on your credit report for seven years.

Not only will charge-offs show up on your credit report, but they can also be very damaging to your credit score.

Did you miss a payment and it showed up on your credit report? This article looks at what you can do to remove a 30-day late payment from your credit report.

You might assume that paying the debt you owe to a collector will automatically remove the mark from your credit report.

Unfortunately, this is not the case.

Negative marks such as collection accounts usually stay on your credit report for up to seven years. This is true even when you have paid them off. Paid charged-off accounts and collections accounts will still show up on your credit report rather than disappearing and will simply appear as 'paid' in their status.

What can you do when there is negative information on your credit report? This guide looks at four simple ways to remove derogatory marks on your credit.

There is a bit of good news on the collections account front, though-- the latest credit scoring models (VantageScore 3.0 and FICO 9) ignore paid collections accounts. If a creditor or lender uses one of these newer models to calculate your score and you pay off the collections account, it won't do nearly as much damage to your score as if you didn't pay the debt.

At this point, though, most creditors are still using the older FICO versions. Collections under $100 are ignored by FICO 8, but all collection accounts are considered in the version most commonly used by mortgage lenders.

If your charged-off account has been sent to collections, take a look at our guide to removing collections from your credit report.