Having a great credit score can allow you to get great deals on credit cards, loans, cell phone plans, apartments, insurance premiums, and more.

If you visit Credit Karma and Experian to find out your credit scores, though, you'll likely find that the two scores you find aren't the same. Why is this?

Experian is one of the three major credit reporting bureaus that compile information about your credit into reports that are used to calculate your credit scores. Credit Karma, on the other hand, isn't a credit bureau and uses information from Equifax and TransUnion to provide free credit scores and credit reports.

Experian is one of the three major credit reporting bureaus that compile information about your credit into reports that are used to calculate your credit scores. Credit Karma, on the other hand, isn't a credit bureau and uses information from Equifax and TransUnion to provide free credit scores and credit reports.While Experian will offer you your FICO 8 score, Credit Karma gives you access to your score based on the VantageScore 3.0 scoring model. The combination of using different credit scoring models and drawing from reports from different bureaus can result in Credit Karma and Experian giving you different credit scores.

Two big names you'll likely come across if you want to check your credit score or report are Credit Karma and Experian.

Credit Karma isn't a credit reporting bureau, but is instead an online service that you can join as a member. Once you're a member, you can receive credit scores and reports along with financial advice and resources. Signing up for a membership with Credit Karma is free.

Here is some basic information about the difference between these two companies:

Credit Karma is an online financial platform and not a credit reporting agency. Creditors don't report to Credit Karma, but, instead, Credit Karma makes credit information easily available to consumers.

You can also access a number of educational and financial tools through this site in order to try and boost your credit scores. This was a privately held company until early 2020 when it was purchased by Intuit.

As a member, you can access your credit reports and scores, which you can save as PDFs or print from their online platform. You can also get a more complete financial picture by registering credit card accounts and bank card accounts. They also have mobile apps for both Android and iPhones.

You can see your Vantage 3.0 scores from both Equifax and TransUnion when you use Credit Karma.

Vantage is a credit scoring model that results from a collaboration between Equifax, TransUnion, and Experian. Your Vantage 3.0 score will be updated weekly as a member, and you can also sign up for credit monitoring alerts that will let you know if there's a change in your score.

There are a number of other credit monitoring services that you can sign up for, which also typically offer credit monitoring alerts as well as identity protection tools and identity theft monitoring tools.

Experian is one of the three major credit bureaus in the United States. Monthly data is provided for each account, including the payment amounts, minimum payment due, and account balances. Using their reports, you can see how much longer your account will show up on your credit file and also detail the monthly balance history for each of your accounts.

Experian is more commonly used for credit reporting by companies than both Equifax and TransUnion. This means that any particular debt or account you have is more likely to show up on Experian reports if they are going to show up on any of your reports.

Operating in 30 countries with 27,000 employees, Experian is a huge company. There are four main business lines: marketing services, credit services, consumer services, and decision analytics.

If you have questions about your credit, you can use the Experian credit hotline in order to talk to an actual person that will help walk you through your report. There are lots of financial resources on their site, including videos and articles, much like Credit Karma.

While Credit Karma offers your Vantage 3.0 credit score, Experian provides a FICO score 8. While there are a number of similarities between the VantageScore 3.0 and FICO 8, they won't produce the exact same number when calculating your credit score.

Though VantageScore and FICO used to use different score ranges, they now both adopt a range from 300 to 850. Higher scores are always better, and both scores are designed to help predict the likelihood that a consumer will repay their credit obligations.

Each of these categories is waited differently, though, meaning that your scores likely won't be exactly the same on both services.

If you are looking to sign up for a service that lets you keep track of your credit scores and reports, Credit Karma and Experian are both popular options.

With Credit Karma, you can sign up for a free membership where you can receive free credit reports, free credit scores, free alerts, and free credit monitoring. When you sign up for the free trial, you don't have to register a credit card.

Credit Karma will also recommend credit cards that you are likely to qualify for, and that could help save you money. The orientation of the site is to help you improve your credit scores, so they'll provide a personalized grade for each of the credit factors and offer suggestions for how you can improve your rating.

There are a number of free options at Experian as well as some paid service packages. For example, you can pay to receive reports from all three major credit bureaus.

Experian's free service, called Experian CreditWorks Basic, offers a number of services for free, including:

Experian CreditWorks Premium comes with a seven-day free trial and then costs $24.99 a month.

Upgrading will give you access to the following features:

There are additional service bundles you can purchase to gain access to even more information and protection. One free service that might interest you is Experian Boost, which lets you add positive payment history to your Experian credit reports from utility and telecom accounts. This can help boost your credit score instantly, though it requires that you hand over some personal financial information.

There are a number of reasons why your Credit Karma score is going to be different than your Experian score.

Credit Karma and Experian offer different scores because they are pulling from different credit reporting bureaus-- Credit Karma provides your scores from Equifax and TransUnion, while Experian provides your Experian credit score.

One reason is that Credit Karma will show you your VantageScore from Equifax and TransUnion, while the free version of Experian will show you your FICO score from your Experian credit report.

Additionally, not all of your creditors and lenders will report to all of the credit bureaus, which can create differences between your reports and your scores.

Every company is going to have its own system and preferences when it comes to pulling credit reports and scores.

In general, though, you'll want to check your FICO Score if you're planning on applying for credit. There's a good chance that lenders will be using this scoring model in order to figure out whether you are likely to pay back a debt you take out.

There are also differences between the various versions of FICO score models. For example, different industries will have standards in regard to which version they use.

If you are planning on buying a house, you'll want to check your FICO Scores 2, 4, and 5, as these are common versions used by mortgage lenders.

Are your credit reports not looking quite as good as you had hoped? Cleaning up your credit report can be well worth the trouble. Make sure you check out our guides to removing collections, hard inquiries, dispute comments, charge-offs, evictions, and late payments if you are ready to improve your credit.

Chances are your credit score will vary depending on which credit bureau is being used to calculate your score. Though people regularly talk about their "credit score," it's usually more accurate to say that each person has multiple "credit scores."

There are a variety of factors that can explain the differences between credit scores from different credit bureaus, including:

Since Credit Karma is an online financial platform but not a credit reporting bureau, you might wonder if the score they offer is accurate.

Credit Karma doesn't collect information from creditors. Instead, they use your credit reports from Equifax and TransUnion to offer scores and reports. The credit calculating model they use is VantageScore, rather than FICO.

The information on Credit Karma should be accurate, but the reality is that they don't share the most commonly used credit scoring model. FICO is much better known than VantageScore and is most widely used by lenders. For this reason, if you're just going to focus on one credit score, it might make sense to work specifically on your FICO score rather than your VantageScore.

Though it can be frustrating to realize that you have two different scores from Experian and Credit Karma, having a healthy credit profile should ensure that your scores are in good shape no matter which credit scoring model is being used or which credit report supplies the information that generates your credit score.

Building credit can take time, but it's well worth the investment of time. When you improve your credit, it can save you tens of thousands of dollars over your lifetime when it comes to the terms and rates you receive for loans, credit cards, insurance premiums, and more.

Are you searching for more resources to help you build your credit and boost your credit scores? If so, make sure you check out our Credit Building Tips blog.

Is Credit Karma Safe?

Is Credit Karma Safe?

Is Creditwise Accurate? Here Are the Facts.

Is Creditwise Accurate? Here Are the Facts.

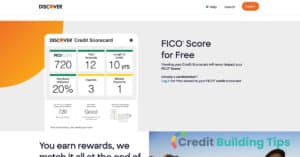

How Accurate is the FICO Score Checker on the Discover Website?

How Accurate is the FICO Score Checker on the Discover Website?

Can You Have a 700 Credit Score With Collections?

Can You Have a 700 Credit Score With Collections?

Credit Bureaus Contact Info: Experian, Equifax, and TransUnion

Credit Bureaus Contact Info: Experian, Equifax, and TransUnion

Why Does a “Factual Data” Inquiry Appear on My Credit Report?

Why Does a “Factual Data” Inquiry Appear on My Credit Report?