Mercedes Benz is one of the most aspirational auto brands out there-- when you own a Mercedes, it's a sign that you've made it in life.

Only the most affluent of car owners, though, can afford the steep price for these vehicles out of pocket.

If you are planning on financing a Mercedes-Benz through their own lending service, you will need a credit score of at least 680. However, you can also obtain a loan from another lender or take out a personal loan, which can allow you to receive financing with a lower credit score.

If you are planning on financing a Mercedes-Benz through their own lending service, you will need a credit score of at least 680. However, you can also obtain a loan from another lender or take out a personal loan, which can allow you to receive financing with a lower credit score.Of course, your credit score and credit report will have an impact on the loan terms you are offered. In order to qualify for a traditional auto loan, you typically need a credit score of at least 600. If your credit score is lower than 600, it's possible to locate a bad credit car loan with much less favorable rates and terms.

There is no standard minimum credit score that you will need in order to apply for a car loan. That being said, each lender will have their own minimum standards that they will apply when they review auto loan applications.

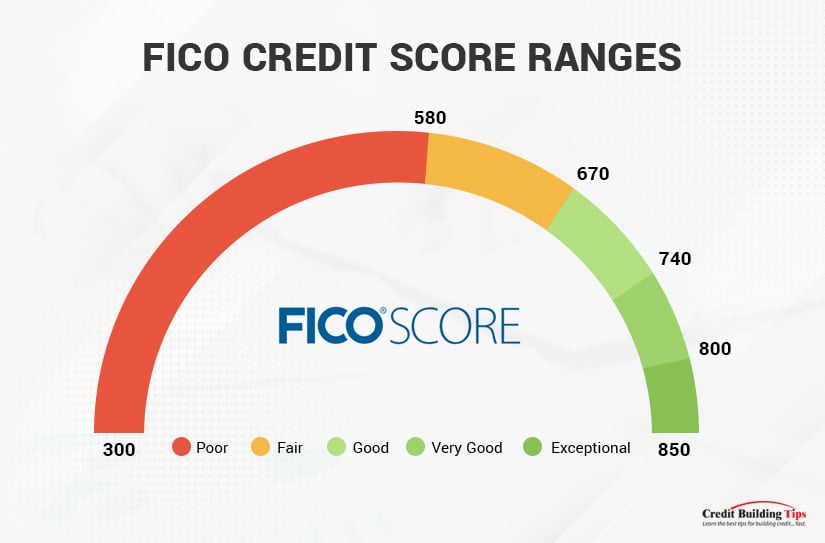

- In general, you will be charged more interest on your loan the lower your credit score. You will typically need to have at least prime credit in order to get a good interest rate on an auto loan. A credit score of 661 or up is considered prime credit in some credit scoring models, while 680 and up is favorable for others.

There are two primary factors that will inform the minimum credit score you need in order to qualify for a car loan:

If a lender advertises a minimum credit score, it doesn't necessarily mean you're out of luck if your credit score is below the listed number. The following conditions might allow you to receive an auto loan from a lender even if your score doesn't meet their minimum:

There are a number of factors that will be taken into account beyond your credit score when you apply for a car loan. In order to determine whether you will be approved and what interest rate you will be offered, lenders will likely evaluate the following:

Though several factors are taken into account when determining whether or not you will be approved for a car loan, your credit score is one of the major factors.

The minimum credit score required for buying a Mercedes Benz with financing is going to depend on the lender that you use. We will go into details about financing using Mercedes-Benz Financial Services a bit later on in the article, but first, let's discuss what you need to know about getting a car loan from any lender for a Benz.

The average cost of a new Mercedes-Benz reached $76,590 in 2022, which is a 43% increase over the average for 2019. This increase has aligned with rising car prices as well as the carmaker's push to focus on top-end models in recent years.

The average cost of a new Mercedes is more than $76,000.

There is no set minimum credit score for purchasing a Mercedes Benz or any particular type of car, for that matter. However, the better your credit score is, the more likely you will be approved and receive favorable terms for an auto loan. This is particularly important when you are buying a car as pricey as the average Mercedes, as higher interest rates will mean paying thousands of dollars than you would if you received the lowest possible interest rates.

You will typically need at least a credit score of 600 to qualify for a traditional car loan, and a score of 661 or higher (sometimes 680 depending on the credit scoring model used) will help you secure a low interest rate.

For example, let's say that you are buying a brand-new Mercedes at the cost of $76,590. You are a prime borrower and therefore receive a low-interest rate of 4.03% for a 48-month loan. You put down 20% as a down payment, which amounts to $15,318.

Not factoring in the cost of sales tax, title, registration, and other fees, this would mean that you would be making monthly payments of $1,384.29 for 48 months. The total interest you would pay over the life of the loan is $5,173.75, meaning that your total cost, including interest, would be $81,763.75.

Receiving financing with a less than ideal credit score can mean that you pay thousands or tens-of-thousands of dollars extra in interest over the life of a loan.

Keeping all of the factors equal except for your credit score, let's now say that you are a non-prime borrower that receives an auto loan interest rate of 6.57%.

In this scenario, your payments would be $1,455.04, and you would pay $8,570 in interest over the life of the loan. The total cost, including interest, for the car would be $85,160.

Finally, let's look at the same example if you were a deep subprime borrower. You receive an interest rate of 12.84%, meaning that your monthly payments amount to $1,638.91. Over the life of the loan, you pay a whopping $17,395.81 in interest for a total cost of $93,985.81.

As you can see, there is a tremendous difference between the amount of interest you pay over the life of the loan depending on your credit score. For this reason, it's worth working to improve your credit score, if possible, before applying for an auto loan.

Has your credit report seen better days? This article looks at four simple ways to remove derogatory marks on your credit.

If you want to get a loan for a Mercedes Benz, you have a few options:

There are pros and cons to each option:

Is there a tradeline on your credit report with the acronym COAF? This stands for Capital One Auto Finance, and you can learn more about how this impacts your score and report in this article.

Receiving financing from Mercedes-Benz Financial Services typically means that you need a credit score of at least 680. If your credit score is below this, you will probably want to shop around for different lenders with less strict credit score minimums.

It's pretty easy to apply for a loan through Mercedes-Benz Financial Services. Here are the steps you'll want to take:

If you want to get an auto loan through Mercedes-Benz Financial Services, you will need a credit score of at least 680 in order to receive favorable loan rates and terms.

If you want to apply for a loan through a different lender, here are the steps you'll want to take:

Are you on a mission to improve your credit so you can buy the car of your dreams? Check out our posts about credit repair hacks to increase your credit score, bank overdrafts and credit scores, repairing credit after identity theft, and removing charge-offs from your credit report.

Auto loans are usually a better choice than personal loans when it comes to financing a car.

This is because:

That being said, you might have your reasons for wanting to apply for a personal loan to purchase a Benz.

To apply for a personal loan, you'll want to:

Did you overdraw your bank account and you're worried it's going to impact your credit score? Check out our post about overdrafts and your credit.

It can be very convenient to receive financing through a dealership when you're buying a car, but it isn't always the best deal. There are other lenders you can use to purchase a Mercedes-Benz, and you will typically receive more favorable rates and terms from a bank, credit union, or online lender.

There are a number of reasons why you might choose to look elsewhere for financing, including:

All that being said, there are some situations where you might actually get a better deal securing financing through a dealership.

These include:

It's generally a good idea to shop around for a car loan before you head over to the dealership. More information is always better, and it will give you a sense of whether the financing the dealership is offering is competitive.

No one likes spending their free time figuring out how to boost their credit score or clean up their credit report, but the truth is that improving your credit can help you achieve your dreams in life.

If you've always wanted a Mercedes-Benz, you're going to need to be approved for a substantial car loan.

Are you ready to improve your credit and purchase the Benz you've always wanted? If so, make sure you check out our Credit Building Tips blog, with tons of resources and articles about credit health.

Reading through your card member agreement as a credit card holder can sometimes feel like you’re trying to translate a different language. If you’re trying to figure out when Discover reports to the credit bureaus and which credit bureaus they report to, it’s easy to start feeling frustrated pretty quickly.

Understanding when credit card issuers report to credit bureaus can help you understand how a late payment can impact your credit and when you should make payments during your billing cycle to ensure your credit score is as high as possible.

Discover, like many credit card issuers, reports to credit bureaus on a monthly basis, usually within several days after the end of your billing period. It is reported that they report to all three major credit card bureaus– TransUnion, Equifax, and Experian.In this article, we’ll explore what you need to know about when Discover reports to the credit bureaus and how you can use this information to your advantage.

Let’s do a quick refresher on how credit reporting works before jumping into the details of when Discover reports to credit bureaus. There are three major credit reporting agencies in the U.S.– Experian, Equifax, and TransUnion.

It is this information that goes into a formula in order to calculate your credit score, which is a numerical score that indicates your financial health. Most creditors report monthly to the credit bureaus, including Discover.

With a revolving line of credit such as a credit card, though, you might rack up a bit of a bill before paying it off on the due date. The tricky thing is that many credit issuers, including Discover, report to the credit bureaus shortly after the billing period has closed but before you’ve made your payment. This can mean that your credit file shows a higher credit utilization ratio than you would expect because the credit card issuer is reporting that you are carrying a balance.

When you want to actively manage your credit score before applying for a loan or credit, it can be useful to make several payments throughout the month so your balance stays low. This way, when the credit card issuer does report to the credit bureaus, your credit utilization ratio will be as low as possible.

Discover reports to credit bureaus on a monthly basis. They do this within several days after the end of a cardholder's billing period. This means that the information that Discover sends to the credit bureaus will be reflected on your credit report a brief period of time after your monthly statement has been issued.

If you are a Discover card member, you can find additional information about how and when Discover reports to credit bureaus under the Credit Reporting section of your monthly account statement.

You will want to note, however, that the date that your payment is due doesn’t always line up with the date that Discover reports to the credit bureaus. This means that it’s possible for you to maintain a zero balance on your card by the end of each billing period– ensuring that you don’t pay any interest and that you aren’t carrying debt from month to month– but your credit report shows that you have a balance on your card.

When Discover reports to the credit bureaus about your credit card activity, the changes can sometimes appear on your credit report immediately. In other cases, though, this new information might not show up on your report for more than a month.

For this reason, it can be useful to learn precisely what date Discover reports to the credit bureau each month so you can make sure you schedule your payments accordingly. You might find that if you make your monthly payments just a few days in advance, the balance reported to the credit bureaus will be more reflective of your actual credit activity and more beneficial to your credit score and file.

It is believed that Discover reports to all three of the major credit bureaus– Experian, Equifax, and TransUnion– about once a month. As stated above, reports are usually made around or just a few days after the monthly billing statement is issued to a card member.

When you are applying for a Discover card, the company might pull your credit report from any of the three primary credit bureaus. That being said, consumer-reported data seems to indicate that Equifax is the bureau they lean most heavily on for sourcing credit reports, with Experian being their second preference followed by TransUnion.

Though it isn’t entirely clear which bureaus Discover uses when pulling credit reports, it seems that their preference can vary depending on the state you are in.

In the following states, it appears that Discover primarily pulls credit reports from Equifax:

It seems that Discover relies on Experian for pulling credit reports in the following states:

Finally, TransUnion appears to be the credit union of choice for the following states:

Of course, you don’t want to assume that Discover will definitively only pull your credit report from one specific credit bureau when you apply for a credit card. It's best to keep an eye on all of your credit reports and make sure they are free of any errors or inaccuracies, particularly if you are planning on applying for a loan or a new line of credit in the near future.

Are there hard pulls on your credit report that aren't accurate? Take a look at our recent post to learn how to remove hard inquiries from your credit report.

Now that you know when and where Discover will report to the credit bureaus, it’s time to take a look at the specific information that they send to Equifax, Experian, and TransUnion on a monthly basis.

The following information will be reported by Discover to the credit bureaus:

Did you find information on your credit report that you don't recognize? Though there are many potential explanations, one possibility is that you've been the victim of identity theft. Check out our guide to repairing your credit after identity theft and fraud.

Your credit limit will be reported to the credit bureaus by Discover when you first open a card with them. This information is important because it is used (along with your account balance) to calculate your credit utilization ratio.

If your limit changes during the time you have an account with Discover, they will report this change to the credit bureau. For example, they might reevaluate your credit file and determine that they want to reduce the amount of credit extended to you. On the other hand, you might request a credit limit increase that is approved by the issuer.

If you do increase your credit limit with Discover, it can take a little time for it to be updated on your credit report. For this reason, you might notice a temporary increase in your credit utilization ratio if you are using more of the credit available to you. Still, your credit limit hasn’t yet changed on your credit report.

Are you worried that a recent bank overdraft is going to lower your credit score? Take a look at our recent post about how overdrafts can impact your credit to learn more.

Understanding when credit card issuers report to credit bureaus can help you time your credit card payments in a way that is advantageous to you. If you always make your payments on the final due date, it’s possible that your credit report always shows you carrying a balance even when you pay your cards off in full each month.

This means that your credit utilization ratio could always be higher than it needs to be. Your credit utilization ratio is considered “extremely influential” to your VantageScore, and it makes up 30% of your FICO score.

FICO and VantageScore are the two most widely used credit scoring models.

Essentially, this means that your credit score could be consistently lower than it needs to be simply because of the timing of your payments and the credit card issuer’s reporting schedule.

Of course, ensuring that your credit score is as high as possible might only be necessary if you are planning on applying for a loan or credit card or if you are otherwise going to have your credit report pulled (for example, by a landlord or potential employer.) Rather than scrambling to try and improve your credit score when you realize your credit report will be pulled, though, it can be easier to time your monthly payments, so they always reflect your true balance at the end of the billing cycle.

There are a number of methods you can use to make sure your true credit card balance is reflected on your credit report every month. By being a bit strategic as to when you make your payments, you can ensure that your credit score is always as high as it can be– at least when it comes to the way your credit utilization ratio factors in.

One thing you can do is make multiple payments throughout the month. You could also choose to set up a series of automatic payments that will withdraw from your account at intervals throughout the month.

If you can get a definitive answer from the credit card issuer as to when they report to the credit bureaus (you might find that a customer service representative can give you a more specific answer in relation to your particular account), you could also set up an autopayment schedule where your card gets paid off in full several days or a week before the issuer reports to the bureaus.

Credit scores, credit cards, and credit reporting agencies are all somewhat mysterious, which leaves most people with a big pile of unanswered questions. Let’s take a look at some of the most commonly asked questions about Discover cards and credit bureaus so you can be armed with valuable knowledge in your quest to improve your credit score.

It is reported that Discover does report to all three credit bureaus. This isn’t just the case for individual and joint account holders but also for authorized users.

Discover reports to the credit bureaus roughly once a month. They typically report around or just after they issue your monthly billing statement.

As a cardholder, it can feel a bit overwhelming trying to learn everything you can about the benefits and consequences of having a credit card. Check out our guides to closing a credit card with a balance, credit card nicknames, and reporting income on credit card applications to learn more.

If you believe that there is information on your credit report that was made in error or is otherwise inaccurate, you can dispute it. You can contact both the credit bureau that is reporting the false information and the credit card issuer. Depending on the error you’ve noticed and whether or not you have an account with Discover, you will also want to make sure that the inaccuracy didn’t appear as a result of identity theft.

Missed payments will usually be reported to all three credit bureaus. However, this typically happens after the 30-day mark, meaning that it has been 30 days since the due date. If you manage to make the payment before they report to the credit bureau, the late payment won’t show up on your credit report. However, you will probably incur some late fees on your account.

Did you have a credit card account get passed over to a debt collector? This type of mark on your credit report can be very harmful to your score, and deleting a collection in exchange for payment is one potential way of repairing your credit report.

Paying a credit card bill one day after the due date often means that you will be charged additional fees for the late payment. However, it shouldn’t show up on your credit report because a creditor like Discover won’t report to the credit bureaus until the payment is 30 days late.

If you do end up receiving a 30-day late payment mark on your credit report, it will likely have an impact on your score. Late payments will stay on your credit report for seven years, but they do become less damaging to your score as they age.

Even if you know that you're going to be a bit late on your credit card payment, it's important that you try to make the payment before thirty days have passed since the due date. Though you will likely incur a late fee, it at least won't show up as a derogatory mark on your credit report.

According to some sources, one late payment will be forgiven by Discover. However, this information can only be found on third-party sites and isn’t available on Discover’s site. If you don’t see that the late payment has been forgiven automatically (meaning no late fees appear on your account), you will need to call and ask if they will be willing to waive the fees since this is your first time being late with a payment.

It’s best not to assume that a late payment will be forgiven, but it isn’t uncommon for creditors to waive the late fees when it is your first late payment. After your first late payment, though, they will be less likely to waive these fees unless you can convince them the late payments have been due to a hardship that you are working to overcome.

If your credit is in really rough shape, there is a Discover card that can help you improve your credit so long as you use it responsibly.

The Discover It Secured Credit Card is a secured card, meaning that you will have to place a security deposit of at least $200. The amount that you deposit becomes your credit line if you end up being approved for the card.

Rebuilding your credit can feel like an incredibly arduous and time-consuming process. If you're thinking about hiring a credit repair service to help you improve your credit, make sure you read our guide to the cost of credit repair services.

There are a number of different factors that go into Discover’s calculation of your credit limit.

These include:

The credit limit offered to you by a credit card issuer is the maximum dollar amount that the lender will allow you to spend. In order to have the best possible credit score, though, you ideally want to be using 30% or less of all of the credit that is extended to you. The ratio of your credit limit in relation to how much of your credit you've used is known as your credit utilization ratio.

It is common for card issuers to report to credit bureaus shortly after a billing cycle has ended. This means that the date that the company reports to these agencies might be days or weeks before your payment is due.

That being said, each issuer can follow its own schedule for reporting to the credit bureaus, though most of them will report every 30 to 45 days. Beyond that, some issuers might only report to one bureau, while others might report to two or all three. Ultimately, it is the decision of the company how they deal with reporting to the credit bureaus.

When it comes to improving your credit, not all tactics are created equal. There are some things you can do that will help boost your score right away, while others can take time to really take effect. To learn more about how to improve your credit score, check out our article with eleven credit repair hacks.

Discover reports to credit bureaus on a monthly basis, usually shortly after a billing cycle ends. They seem to report to all three credit bureaus, but which credit bureau they will pull a credit report from seems to vary by state.

It's easy to get frustrated with the entire credit system-- why should you need to know exactly when Discover reports to the credit bureaus?

In truth, though, having this type of knowledge can make a big difference in your credit score when you're applying for a loan. If a creditor like Discover reports your account information when you're balance is at its highest, it's going to make your credit utilization ratio higher than it needs to be.

Similarly, understanding when they report to the credit bureaus can help you determine whether a late payment is going to show up on your credit report. Making sure you pay any late payments before thirty days have passed since the due date is important if you want to keep your credit in tip-top shape.

Are you on a journey to improve your credit? If so, make sure you check out our Credit Building Tips blog for more tips, tricks, and resources.

Signing the back of a credit card was once a key step consumers could take to prevent credit card fraud. These days, the ability to electronically (and securely) authenticate credit card purchases makes it so the signature on the back isn't quite as important.

That being said, some credit issuers still require cardholders to sign the back of their card in order for it to be considered active and valid.

If you've ever signed the back of a card with whatever pen you have lying around, you've probably noticed that the signature smudges or wipes off with use. In this article, we'll look at what you need to know about choosing the best pen to sign a credit card or debit card so it is both legible and long-lasting. (Hint: the answer is an ultra fine-tip permanent marker!)Without further ado, let's explore the question of which pen to use to sign the back of your card.

We’ve all been there– you received your new card in the mail and activated it using the authorization number. You flip your card over and sign your name, only to find that your signature smudges or even completely wipes off after just a few uses.

Luckily, the answer is yes.

When searching for the perfect pen for signing your credit card or debit card, look for the following features:

If you’re going to go out and get a pen to sign your card, the best choice is going to be an industrial fine-tip Sharpie marker. A regular, fine-tip, or ultra-fine-top sharpie can also work in a pinch, as well as fine-tip markers that are designed for labeling DVDs and CDs.

If you’re looking for a bit more guidance than that, don’t worry. We’ve got you covered!

Here are some pens that will help create a smudge-free signature that doesn’t wear away after a few swipes:

Did you get a new debit card, and you're wondering if your recent overdraft is going to ding your credit score? Check out this article to learn about whether bank overdrafts impact your credit.

Most people have a collection of different types of pens sprinkled around their house– ballpoint pens, fountain pens, felt-tipped pens, and gel pens. Let’s look at how each of these can work for signing your cards.

Ballpoint pens can smudge easily when you use them to sign the back of a debit or credit card. Even if they don’t smudge right away, they can rub off over time with use.

If you do end up using a ballpoint pen to sign the back of your card, you’ll want to make sure that your signature dries completely before you stick your card in your wallet.

Fountain pens aren’t a good choice for credit or debit card signatures. The ink from fountain pens can be easily wiped off or smudged because of the way water-based ink interacts with the smooth surface of the card.

Getting a new credit card can be exciting, but there can also be a lot to learn as a new cardholder. Check out our guides to closing a credit card with a balance, credit card nicknames, and reporting income on credit card applications to learn more.

The best pens you can use for credit card signatures are permanent markers, as they dry quickly and don’t smudge or wear off the same way other types of pens do. However, many permanent markers have a big, chunky tip, which won’t work well for the thin signature strip.

When choosing a permanent marker to sign your card, look for one with a fine or ultra-fine tip. This way, your signature will be easily readable.

Gel pens are probably the worst type of pen to use on a credit or debit card. The nature of the ink means that it doesn’t adhere easily to the plastic card, and the ink will likely smudge or rub off quickly. The ink doesn’t dry quickly on such a slippery surface, meaning that you really don’t even want to use this type of pen in a pinch.

If this is your very first credit card, you might be unsure of how the whole process works and what it means for your credit report. You can learn more about the tradelines on your report and how long they stay there in this recent post.

You should always use black ink to sign the back of your credit or debit cards. Though black and blue ink is often considered acceptable for financial and official documents, it’s possible that signing your card with blue ink could actually invalidate the card. If you have your heart set on using blue ink, you’ll want to check with your debit or credit card issuer.

The material that credit cards are made out of is quite slick, which means that not all ink will easily adhere to it. Using the wrong pen to sign the back of your credit card can mean that your signature smudges right away.

In order to have your credit card signature remain legible and clear for years to come, you'll want to use a felt-tipped pen. Using a pen with a fine or ultra-fine point will ensure that your signature is written in a way that is easily readable.

When you get your new card, the last thing you want to do is somehow invalidate it by not signing it properly. Let's take a look at the answer to some of the most common questions asked about signing credit and debit cards.

Signing the back of your credit card was once an essential step in preventing the occurrence of credit card fraud. Back in the day, the merchant would compare the signature on your card to the signature on the receipt when you paid with a credit card. If the signatures were a match, the transaction would be approved by the merchant.

Here in the present day, authentication occurs electronically. This means that it isn’t nearly as important to sign your credit card as it once was.

That being said, some card issuers still require that your card is signed. In these cases, your signature can be an indication that your card is active and that you are on board with the credit card agreement terms.

You might even find that one of the cards in your wallet says something along the lines of:

Considering that a card that isn’t signed could be viewed as invalid or inactive by a merchant, it’s possible that your card could be refused if there isn’t a signature on the back. When in doubt, it’s a good idea to check with your credit or debit card issuer to see if it’s necessary for you to sign the back of your card.

Did someone get a hold of your credit card information and wreak havoc on your credit score? This guide goes over how to repair your credit after identity theft and fraud.

Some cardholders will write “See ID” in the signature strip rather than actually signing their name. Is this a good idea?

The reason that people do this is that it theoretically decreases the chance of being a victim of credit card fraud. The idea is that when the merchant goes to check their signature, they are prompted to ask for ID before continuing with the sale. If someone fraudulently got a hold of the cardholder's credit card, they wouldn’t be able to produce an ID that matches the name on the card.

While this might seem like a worthwhile layer of protection between you and credit card fraud, there are a few issues with this strategy:

If you are interested in writing “See ID” instead of signing, you’ll want to contact your issuer or take a look at your credit or debit card agreement.

Speaking of keeping your credit card info safe and secure, have you ever wondered what that three or four digit number is on your credit card? Take a look at our guide to CIDs on credit cards to learn more.

This depends on whether or not the card issuer requires that your card is signed in order for it to be considered active and valid. If your issuer doesn’t require a signature, you are free to leave the signature strip blank if you so choose.

These days, some cards don’t even have a signature box if the issuer doesn’t require it. If this is the case, you certainly don't have to sign.

Are you considering applying for a new credit card but you're also planning on applying for mortgages soon? Take a look at our article about whether it's a bad idea to open a new credit card before buying a house to look at both sides of the argument.

When you receive a new credit card or debit card, flip it over to look at the back. There should be a blank, white strip. This is what is known as the signature bar, and it is where you should sign your card.

Don't worry-- this doesn't mean you received a defective card. Card issuers have started phasing out the signature strip as retailers have been moving away from requiring signatures. Transactions can now be authorized through the EMV chips in your card, meaning that the signature doesn't play the same crucial role it once did in preventing credit card fraud.

If there's no signature strip, it means you don't have to sign your card.

If you want to change the signature on the back of your debit or credit card, you will want to request a new card. This will allow you to create a fresh signature on the back that matches the signature you use during transactions.

It's generally advised that you sign your name in cursive instead of simply printing your name on the back of your card. The reason for this is that it is typically harder to forge a distinct cursive signature than a printed name.

When you sign the back of your card, you want your signature to be identical to the way you would sign your name on a receipt or on any other document. This means that if you normally include your middle name in your signature, you'll want to do the same on the back of your card.

Technically, some credit card issuers require that your card is signed in order to be valid and active. Others, however, don't even require that you sign your card anymore.

It isn't important that your signature is legible on your card-- many people have signatures that are very difficult to read. What is important is that it matches your typical signature on other legal documents. If you are concerned about legibility because the signature is wiped off or smudged, you'll want to use an ultra-fine felt-tip pen to ensure it is permanent and easy to read.

When your brand-new credit or debit card shows up in the mail, the first thing you'll want to do is activate it. You can easily do this online or over the phone, and the information you need to activate your card should be included on a sticker on your new card.

This sticker will give you the instructions you need to follow to activate your card. Once your card has been activated, it's time to sign the card (if there is a signature strip where you can do so.)

The question of which pen to use to sign the back of your card might seem like a minor issue, but it's details like these that add up to create a healthy and stable financial life. Though signing the back of your card might not be required by all card issuers, it's still possible that it could provide some added security for you against credit card fraud. Beyond that, some credit card companies actually require that you sign your card in order for it to be considered active and valid.

It's possible, in this case, that you could end up having a transaction declined because your card is considered invalid and inactive without a signature. Even if you did sign it once, a signature that wipes off over time could eventually cause you some trouble.

Are you working on getting your finances in order and rebuilding your credit? If so, you've come to the right place. Make sure you check out our library of resources over at our Credit Building Tips blog to help you boost your credit quickly and effectively.

Your checking account is a central part of your financial life. For this reason, you might assume that overdrawing your account could have an impact on your credit score.

The truth is, though, that normal day-to-day use of your checking account won't show up on your credit report as you aren't spending money that you borrowed from someone else. Instead, when you use a debit card, write a check, use an ATM, or otherwise use your checking account, you're simply drawing upon your own stash of cash.

Bank overdrafts and other checking account activity won't appear on your credit report. However, if you do not pay your overdraft fees or return your account to a positive balance after an overdraft, the debt can be sent to collections. Collection accounts appear on your credit report and can have a serious impact on your credit score.Let's take a look at what you need to know about overdraft fees and your credit score to ensure that your score stays as healthy as possible.

Your credit report displays information about your current credit situation and your credit activity. This means that information about your credit card accounts will show up on your credit report, including 30 day late payments.

However, a debit card isn't using money that you're borrowing-- it's taking money out of the checking account you have with a bank.

This means that checking accounts aren't one of the accounts that are listed on your credit report. The same is true when you use a debit card to withdraw money from an ATM, write a check, withdraw money in person, or have automatic payments withdrawn from your checking account.

When you use a debit card, you aren't borrowing money from anyone but instead using the money you have in your checking account. This means that checking accounts don't show up on credit reports.

Information about your checking accounts won't appear on your credit report unless a financial institution sends your account to collections for unpaid overdraft fees or negative balances.

When you make a payment using your checking account, but there isn't enough money in your bank account to cover the cost, banks will sometimes still pay the transaction.

There are a number of ways you can overdraw your checking account, such as through debit card, ATM transactions, checks, electronic or in-person withdrawals, or automatic bill payments.

There are lots of banks and credit unions that offer programs known as overdraft protection programs.

If you spend more money than there is in your checking account and your bank covers it, you might incur an overdraft fee.

It's worth knowing that there is an organization called ChexSystems-- a bank reporting bureau-- that does keep an eye on your checking and savings accounts with credit unions and banks.

Items like overdrafts, unpaid negative balances, bounce checks, fraud related to your account, or involuntary account closures will be tracked by ChexSystems.

If your ChexSystems report shows that you have used bank and credit union accounts irresponsibly in the past, you could be denied when you apply to open a new bank account.

If you're denied opening a new bank account because of your ChexSystems report, this can obviously cause a number of problems for you financially. That being said, it won't impact your ability to get a new credit card or take out a loan, and it won't affect your credit score.

There is one circumstance where your credit score could be hurt by an overdraft-- if it is sent to a collection agency.

Are you worried you won't qualify for a loan because you have too many recent hard inquiries on your credit report? Check out this guide to removing hard inquiries from your report.

If your bank or credit union covers the cost of a transaction for you via overdraft protection, you will have fees and a negative balance to pay. If you pay these, it won't have any impact on your credit score.

However, if you don't pay the fees or your negative balance, the financial institution might send your debt to a collection agency. Once an account has been created for you with a debt collector, it can end up appearing on your credit report.

It's, therefore, essential that you cover any negative balances you have as well as any overdraft fees right away. This is the only way to avoid the account being sent to collections.

If your credit dropped dramatically over a short period of time, check out our post about why you might experience a large drop in your credit score.

It will negatively impact your credit score if your account is sent to collections for unpaid overdraft fees or negative balances.

The longer you have unpaid debt in collections, the more derogatory marks you will accrue on your report. This is because late payments appear in a number of categories, such as 30-day, 60-day, and 120-day late payments.

Having a debt in collections is one of the most severe derogatory marks you can have on your credit report. This is because the original creditor has written off recouping the debt and has passed it off to a collection agency.

The best way to avoid this situation is to make sure your accounts are current before they get to the point of reaching collections. Ideally, any money you owe will be paid before thirty days have passed, as financial institutions usually report to credit bureaus once payment is thirty days late.

If you already have debts in collections, make sure you check out our post about how to delete collections from your credit report.

Overdraft protection can be a useful safety net, but you might choose to opt out of the program if you are consistently overdrawing your bank account. This is because it can mean paying a lot of money in overdraft fees in aggregate.

Though this can be uncomfortable or embarrassing when you go to make a purchase, it does mean that you aren't racking up overdraft fees.

Another thing you can do to provide overdraft protection for yourself is to link your checking account with a savings account. If you don't have enough money in your checking account to cover a purchase, the money will be moved from the account that you linked to your checking account.

It's worth noting that your bank might still charge you a fee for moving money from a savings account to a checking account to cover the cost of the transaction. In most cases, though, the fee is much lower for linked accounts than when the bank or credit union is covering the cost for you.

Avoiding overdrafts is the best way to avoid negative marks on your ChexSystems report as well as the potential for your account to be sent to collections for unpaid negative balances or overdraft fees.

Many banks and credit unions offer a number of different options for overdraft protection.

For example, some offer:

If you are frequently incurring overdraft fees, the best choice might be to opt out of overdraft protection completely. Though this means that your transaction will be declined, it does ensure that you aren't spending money you can't afford to pay back.

One useful tool you can use to avoid overdrafts is to sign up for an alert system if your bank offers one.

Low balance alerts can help you stay aware of when you might not have enough money in your account to cover a transaction. This can either indicate to you that it's time to transfer money into your account or to slow down on your spending.

Are you suffering from imperfect credit because someone stole your identity? Make sure you check out our recent post about how to repair your credit after identity theft and fraud.

A number of major banks in the United States have begun implementing policies to eliminate overdraft fees.

These include:

Other banks have started introducing new financial products without overdraft fees.

You might find that opening a checking account with one of these institutions is a useful strategy. Make sure you take a look at our list of the best "no overdraft fee" checking accounts.

Though overdrawing your checking account might not have a direct impact on your credit score, there are still a lot of reasons why you want to avoid spending more money than you have in your checking account.

Beyond that, if you don't settle a debt you owe to a bank for accrued overdraft fees or negative balances, the debt can end up being sent to collections. This will almost certainly have a negative impact on your credit score and make you seem like a riskier borrower to lenders.

For these reasons, it's generally a good idea to come up with a plan to avoid overdrawing your checking account. If you do end up spending more than you have in your account and your bank covers the cost, make sure you bring your account back to a positive balance and pay any overdraft fees right away. This way, you can avoid them being sent to collections.

Is it time for you to improve your credit score and clean up your credit report? Make sure you check out our credit-building tips blog for more resources that will help you boost your credit.

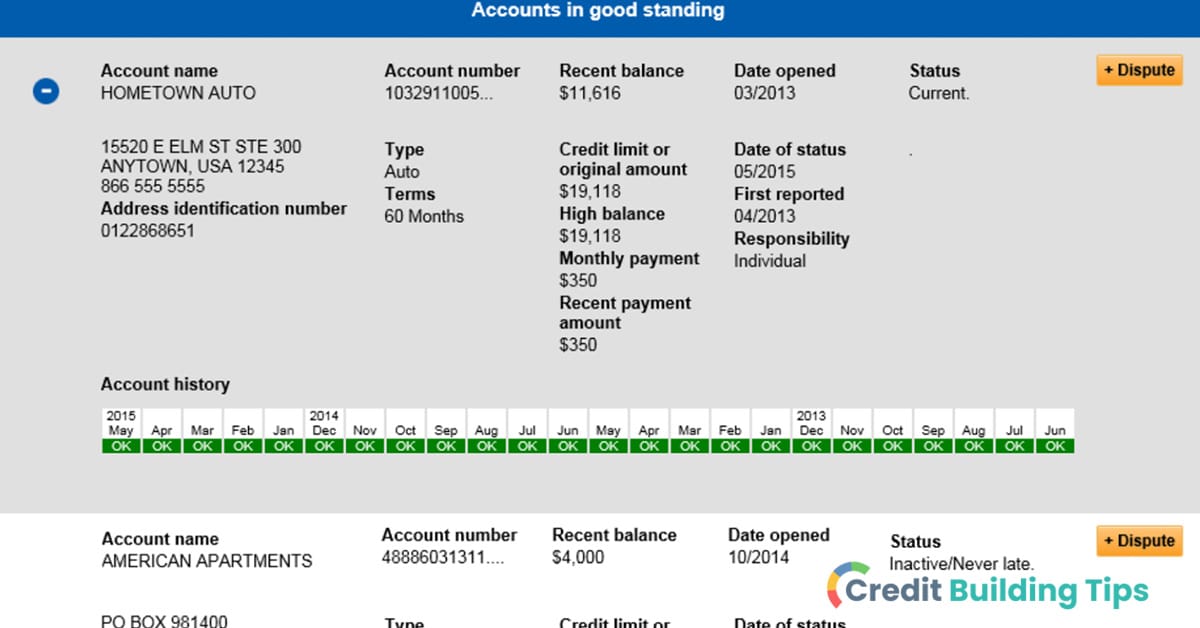

When credit bureaus refer to accounts on your credit report, they call them "credit tradelines." There are three different types of tradelines that can show up on your report-- revolving accounts, installment loans, and open accounts.

How long do tradelines stay on your credit report? How does it affect your credit when a new tradeline is added or removed from your file?

Tradelines will usually stay on your credit report for seven to ten years after they have been closed, and will remain on your credit report so long as they are open and active.How long a credit tradeline stays on your credit report depends on a number of factors. If you need a refresher about what exactly a tradeline is, skip down to the next section of the article.

Tradlines will stay on your credit report for at least seven years if not longer.

Any open and active accounts will have tradelines on your credit report. Once an account is closed, how long it remains on your report depends on whether it was closed in good standing.

When you close an account in good standing, the tradeline will usually stay on your credit report for ten years. However, it is ultimately up to each reporting agency to decide how long tradelines are maintained.

When an account is closed in bad standing, it will stay on your credit report for seven years.

There are a few exceptions to this rule– for instance, negative tradelines might remain on your credit report for ten years if they were resolved via certain types of bankruptcy.

Essentially, accounts in good standing will stay on your credit report longer than accounts in bad standing once they are closed. This means that your past positive history will have an impact on your scores and file for a longer period of time than your past negative history.

The credit bureau has a term for an account on your credit report– a credit tradeline. There are three different types of tradelines that you’ll want to be familiar with:

Each of your credit accounts will have a separate “tradeline” on your credit report. These include detailed info about your payment history as well as the nature of the account.

It’s important that the information in your tradelines is accurate because it is used to determine your credit score.

There are a number of important elements you’ll want to know when it comes to your tradelines if you’re hoping to build and maintain a healthy credit profile, including:

Understanding this information can help you make more informed financial decisions in order to keep your tradelines positive as well as boost your credit score and establish a good credit history.

You can learn more by reading our comprehensive guide to how tradelines work.

Every account that you have is considered a single credit tradeline. Whether you are up to date with your payments or behind, whether it’s a solo account or a joint one, or whether the account is open or closed, each one is considered its own credit tradeline.

There are three categories that tradelines can fall into: revolving accounts, installment loans, and open account. Let’s take a closer look at each of these.

A revolving account is a particular type of credit account that offers a borrower a maximum limit. Credit cards and lines of credit are both examples of revolving accounts.

Where does this name come from, you ask? These accounts are known as “revolving” because the following information can continue to change as you make both purchases and payments:

Installment loans are accounts where you borrow a fixed amount of money from a lender and follow fixed terms during repayment. Student loans, personal loans, auto loans, and mortgages are all considered installment loans. However, some credit experts believe that mortgages should exist in their own fourth category.

Open accounts are accounts that are payable in full when the consumer receives something of value, such as merchandise. These aren’t nearly as common for individuals and are more common on business credit reports.

Ready to start improving your credit score and reports? Check out our guides to removing late payments incurred during the pandemic, removing evictions from your credit report, opening a new credit card, and hiding credit card utilization.

Both the weight and elements of tradelines are going to be different between each category. For instance, your credit score will most likely be much more impacted by falling behind on an auto loan or mortgage as opposed to missing a credit card payment.

Another important difference is that revolving account tradelines will include both your credit limit and utilization. This information isn’t something that will appear for an installment loan tradeline.

There is a tone of information given with each tradeline. The reason for this is in order to help lenders and creditors minimize risk when they make lending decisions.

Some of the information you might find under a credit tradeline include:

Lenders and creditors are the ones that determine the information they provide in tradelines, so you might find that some tradelines or some specific information don’t show up on your reports.

Your credit score is calculated using the information in your credit tradelines. Actually, in order to even have a credit score you need at least one tradeline that’s been active during the prior six months.

Your score is calculated using each element of every tradeline on your report. That being said, they aren’t all incorporated with the same amount of weight.

For instance, using the FICO scoring model, your payment history has a bigger impact on your credit score than the types of accounts you have.

When you apply for a loan or line of credit, creditors and lenders have free rein in terms of which details they use in order to gain a greater understanding of your financial situation. For example, you might be less likely to be approved for an installment loan if the lender sees that you have received a number of late payment marks on your credit report recently.

On the other hand, a series of late payments a few years back might be seen by a lender as evidence of a previous setback that won’t affect their lending decision because the consumer has remained current on all of their accounts for several years.

Removing a tradeline from your credit report can sometimes have an impact on your credit scores, but what type of tradeline it is and whether you were just an authorized user or the owner can impact whether or not it has any influence on your score.

Your credit credit score can be affected by closing a revolving credit account for a few different reasons.

The first is that your credit utilization ratio will increase because you lose the available credit limit on the account. A higher credit utilization ratio is a sign of risk to creditors and lenders, because it means you’re using a higher percentage of the credit that is available to you.

Ideally, you want to keep your credit utilization ratio below 30% and the lower is usually the better.

The second is that the average age of the accounts on your credit report can be lowered by closing a credit card account, which is one of the factors used to determine your score. That being said, an account in standing will stay on your report for about ten years, which means this shouldn’t be cause for immediate concern.

When you close a credit card account, you might notice that your scores decrease initially but then rebound in a few months so long as you maintain a positive payment record. It’s generally advised not to close a credit card account if you are planning on applying for financing or other credit in the next several months.

Paying off installment loans can lower your credit score. This might seem a bit unfair at first, but you’ll be glad to know that this is typically only a temporary reduction.

Our credit scores can change on a day-to-day basis as we add and subtract money from the loans and debts that we have. When you take out an installment loan, you agree to a specific interest rate and pay-off terms. This includes the date on which you will need to have completely paid off the loan. According to the loan agreement, you will make monthly payments of a certain amount.

It can contribute to your positive credit score and credit mix when you make on-time monthly payments to your installment loan. When your loan is paid off in full and you are no longer making monthly payments, this can lead to a slight temporary reduction in your scores.

That being said, assuming that all else is well with your credit file and you have other accounts with positive payment histories, your score should recover rather quickly.

You can learn more about whether installment loans can help rebuild bad credit in this guide.

A "credit tradeline" sounds more complicated than it is-- it's simply just the term that credit bureaus use to refer to each account that you have established with a lender or creditor.

There are three national credit reporting agencies-- Equifax, Experian, and TransUnion. You can get a free copy of your credit report from each credit bureau from AnnualCreditReport.com, a site authorized by Federal law.

When you look at your credit report, you can see detailed information about each account under each tradeline. This includes both your positive and negative payment history.

The information that is found in your tradelines is used to calculate your credit score. Lenders can look at these details as a part of deciding whether or not they feel it is risky to lend you money.

Tradelines will remain on your credit report as long as they are open and active, and then will stay on your credit report for at least seven years after the accounts have been closed. Accounts with positive histories usually stay on your report for ten years, while accounts with negative histories will stay on your report for seven years in most cases.

Considering how important the information is in your tradelines, you can see why it's so vital to regularly review your credit report to make sure that all of the info listed is accurate. If you're on a mission to improve your credit file, make sure you check out our credit building blog.

Are you looking to rebuild your bad credit score? Installment loans may be the solution you're looking for and you're about to learn exactly what steps to take to get started right now.

Installment loans are a great way to help you pay off debt, fix bad credit, increase your credit score in general, and get back on track financially. I've personally used them in the past to help my own credit score.In this blog post, we'll discuss the benefits of using installment loans to rebuild your bad credit score and how to go about it. We'll also provide tips and strategies to help you make the most of your loan and keep your credit score rising.

An installment loan provides a borrower with a fixed amount of money that must be repaid in regular payments over a period of time. Each payment includes repayment of a portion of the principal amount borrowed and payment of interest on the debt.

The main variables that determine the size of each loan payment are the amount of the loan, the interest rate charged by the lender, and the length or term of the loan. The regular payment amount, typically due monthly, stays the same throughout the loan term, making it easy for borrowers to budget for their required payments in advance.

Installment loans can also offer better terms than other forms of financing, such as payday loans, and can help individuals build their credit score if they make all payments on time. This can make them an excellent choice for those with bad credit who want to rebuild it.

They are closed-ended debt products — you get the loan fund as soon as you're approved and then pay the loan off every month for a predetermined loan term. They're a "handy personal finance tool" that lets you pay off a considerable debt in "small, manageable chunks."

When you take out an installment loan, your lender will do a hard credit check, which can temporarily lower your score. However, if the loan is from a reputable lender, they will report all on-time payments to at least one of the three major credit bureaus.

Payment history makes up 35% of your FICO score, and regular, on-time payments can help build it up. Late payments can greatly impact your score, with even one 30-day or more late payment knocking off up to 100 points.

Most lenders have the option to set up automatic payments, so you don't have to worry about forgetting to pay. This removes the pressure and ensures that your credit score will benefit from regular payments.

The other 65% of your FICO score comes from the amount of debt you owe (30%), the length of your credit history (15%), and new accounts/inquiries (10%). An installment loan can also improve these factors by providing you with access to additional funds when needed.

As long as you use the money responsibly, not maxing out your available balance, an installment loan can increase your available credit score without creating too much debt. You need to be careful not to rack up any additional debt while trying to rebuild your credit score; only borrow what you need and make payments regularly and on time to see positive results.

Try to keep your credit utilization low — ideally below 30%. This means having balances that are no more than 30% of your overall available credit limit. If you're able to keep your utilization low and consistently make payments, then using installment loans for bad credit can help you rebuild your credit score over time.

Staying on top of managing your finances with budgeting and tracking expenses may give you added peace of mind knowing where exactly your money is going each month. By doing this, you may even find opportunities to save more money and allocate those funds towards paying down existing debt or growing your savings account.

Installment loans are a great way to rebuild your credit score, as they can be an effective tool for repairing bad credit. With an installment loan, you can make a series of payments over a period of time that can help you improve your credit score.

The major advantages of installment loans include the following:

Flexible Repayment Plans: Installment loans typically come with flexible repayment plans that allow you to spread out the cost of the loan over an extended period of time. This makes it easier to manage your payments and, in turn, helps you to improve your credit score better.

Lower Interest Rates: Because installment loans usually involve smaller amounts of money and require regular payments, lenders may be more willing to offer lower interest rates. This can help you save money in the long run as you will pay less interest over the life of the loan.

Predictable Payments: Unlike other types of loans, installment loans require regular payments, which makes them much easier to plan for and manage. This also helps reduce the risk of falling behind on payments, as you will always know exactly how much you must pay each month.

Faster Results: Since you will make regular payments on an installment loan, this will help you build your credit score much faster than if you were just trying to pay off a lump sum loan at once. This is why many people choose to use installment loans when they are trying to repair their bad credit scores.

While taking out an installment loan can benefit someone with a bad credit score, there are some risks associated with it. First, you need to consider the amount of money you're borrowing. If you take out a loan that's too large for your budget, you may struggle to make the payments on time, which could further damage your credit score.

You should also consider the interest rate. Installment loans tend to have higher interest rates than other types of loans, so you should make sure you can afford to pay the total amount you borrowed. This is especially true if you're taking out a longer-term loan with a high-interest rate.

If you fail to make payments on time, your loan may go into default, which means that you'll be responsible for paying late fees and any additional costs associated with the loan. This could put you in a worse financial situation than when you started.

It's important to weigh the pros and cons of taking out an installment loan before making a decision.

While installment loans can help rebuild your bad credit score, it's important to make sure that you understand the risks and can afford to make all of the payments on time.

There are many types of installment loans, including personal loans, auto loans, student loans, buy now, pay later loans, no-credit-check loans, and mortgages.

Personal loans are unsecured loans that are generally used for larger purchases such as home improvement projects, debt consolidation, medical bills, or starting a business. Personal loans typically offer repayment flexibility and hardship payment relief, making them more desirable than credit cards.

Unlike secured loans, unsecured loans allow you to borrow money outright (after the lender considers your financials). Secured loans are backed by some type of security, and the lender places a lien on the asset you offered as collateral. Once the loan is repaid in full, the lien gets removed.

Auto loans are typically secured by the vehicle you are purchasing and often come with in-house financing and refinancing options.

Auto loans usually have lower interest rates and longer repayment periods than credit cards.

Student loans are offered by the federal government and online lenders. Student loans typically have flexible repayment options and low-interest rates.

They affect your debt-to-income ratio (that's the amount of debt you owe compared to your total income). If this ratio is abnormally high, it could affect your ability to qualify for any additional credit.

Buy now, pay later apps are offered by most retailers, especially online retailers. These apps allow you to make purchases without using your credit card and then pay them off in installments over time. They also often include promotional discounts and other incentives to encourage customers to use their services.

According to Investopedia, the best buy now, pay later apps of 2023 are:

These types of loans are often extended by payday lenders and don't require a credit score check. They're meant to help consumers with a small personal loan, usually limited to $500.

Payday loans are borrowed against your next paycheck, where you give the lender a check that's postdated for the amount you are borrowing. Once you get your next paycheck, the lender will cash your check. These loans are short-term and charge hefty fees for the privilege.

Mortgages are generally larger loans used to purchase a home.

Mortgages can come with fixed- and adjustable-rate options, larger loan amounts, government-insured mortgages, and conventional loans.

Finding the best installment loan for your needs can be daunting, especially if you have a poor credit score. However, it is important to shop around and compare lenders to get the most favorable terms.

When looking for an installment loan, looking for a lender willing to work with you despite your credit score is important. You should look for a lender who offers competitive interest rates and fees, as well as flexible repayment terms. Don't forget to read through the fine print of any loan agreement to ensure no hidden fees or costs.

It's also important to research lenders carefully. Check out the company's reputation online and make sure they are accredited by the Better Business Bureau. Ask friends and family who they have used in the past and read reviews from other customers. This will help you narrow down your list of lenders and make sure that you are dealing with a reputable lender.

Consider talking to a financial advisor about your options. A financial advisor can help you weigh the pros and cons of different loans, negotiate better terms, and determine if an installment loan is the right option for you. With their help, you can make an informed decision about the best loan to meet your needs.

Once you find a suitable installment loan, it's important to stay current on payments so that you can begin rebuilding your credit score. Make sure you pay at least the minimum payment amount each month and try to pay more if possible.

Paying on time each month shows creditors that you are responsible and reliable, which can go a long way toward improving your credit score. Additionally, keeping track of your spending is essential when taking on new debt, so set up a budget plan before taking out an installment loan.

Keep in mind that rebuilding bad credit takes time. If you stick with your payment plan, make smart financial decisions, and remain patient, you will eventually see improvements in your credit score over time. With hard work and dedication, you can use installment loans to rebuild your bad credit score and achieve the financial freedom you need.

When considering an installment loan to help rebuild your bad credit score, it's important to look at all of your options.

One option is to use a line of credit or credit card. This offers more flexibility than an installment loan, as you can make interest-only payments during the draw period. Credit cards offer perks like cash back and travel rewards, but their high-interest rates can be avoided by paying back what you spend at the end of the billing period.

Another alternative to an installment loan is a home equity line of credit (HELOC). This is the best option if you need to cover a series of major expenses.

Lines of credit and credit cards are best for frequent expenses, while installment loans are best for one large expense. An advantage of an installment loan is that it has fixed interest rates, which helps with budgeting for the future.

It is important to carefully consider all of your options when making decisions about how to finance a purchase or rebuild your credit score. While an installment loan may be the best choice for some, other options like lines of credit and credit cards can offer greater flexibility and additional rewards.

An installment loan may be the best choice if you have one or more big expenses to cover. And as with all things related to credit, paying your loans on time and in full is the absolute best way to build your credit score.

Once you get into this habit, you'll qualify for low-interest rates and have the ability to finance the purchase of a home or car on credit.

When you open a credit card account, the creditor assesses the likelihood that you will be able to pay back the debt. What happens if something unexpected happens and your circumstances change, though? What happens if you’re struggling to make your payments or you’re behind on the debt?

If you’re dealing with an event or a circumstance that has impacted your ability to pay, you might consider writing your creditor a hardship letter.

You can send a hardship letter to a credit card company when you’ve dealt with a hardship that makes you unable to make a payment on time, such as a serious illness, job loss, or natural disaster. This letter explains the hardship you went through, the plan of action you are asking the credit card company to take, and has substantiating documents attached.A hardship letter is a letter you can write to a lender that explains the circumstances that made you unable to make your payments on time. Included in this type of letter are the specific details about when your hardship started, what the cause of the hardship was, and when you expect to begin making regular payments again.

This is also an opportunity for you to express how you want your lender to help and how the solution you are proposing would benefit them.

There are a number of types of relief you might ask for in a hardship letter, including:

For instance, you might communicate to your lender that you will be able to avoid going into default if they are willing to reduce your interest rate for a certain number of months. In this scenario, you could explain to them that you believe you will be able to start making regular payments at the current interest rate after that period of time.

While the dictionary might define “hardship” as severe suffering, lenders are only going to consider certain events to be hardships. In their view, hardships are negative events that harm your finances that are outside of your control.

Some examples of occurrences that a creditor might deem financial hardships include:

Hardship events don’t necessarily have to happy directly to you for a creditor to consider altering their agreement with you. These occurrences can also happen to individuals that you either take care of or rely on.

For instance, if your child were to fall seriously ill in a way that you took on increased medical debt and had to work less hours, a creditor could understand this situation as a valid hardship.

On the other hand, lenders likely won’t consider the following to be financial hardships:

For more in-depth information about credit cards and your credit, check out our recent guides on closing a credit card with a remaining balance, opening a new card before buying a house, and properly reporting income on credit card applications.

Before you start drafting your hardship letter, you’ll want to determine whether or not this is the right way to try and communicate to the credit card company. You might find that your creditor actually provides all of the info that you need online to request hardship assistance.

For instance, American Express has a page on their website that gives clear instructions regarding how you can request financial relief in the form of temporarily lower interest rates and monthly payments.

You’ll want to login to your credit card account online to find out if the credit card company that you want to negotiate with has an easy and already-existing process you can go through in order to request assistance.

Some individuals also might prefer to talk to a customer service representative through online chat or by making a phone call. Even if you aren’t going to be emailing a hardship letter or sending one through the mail, it can be useful to write a simple script for yourself to make sure you hit all of the most important points. This doesn’t necessarily need to be a word-for-word script, but rather a list of essential bullet points.

If you have dealt with a hardship and need to seek financial help for your family, you can learn more about government benefit assistance programs at the U.S. Department of Health and Human Services site.

How should you go about drafting a hardship letter? What will you want to keep in mind as you're writing? These tips will help you create a letter that gives you the best chance of receiving a favorable response.

When you are overwhelmed by your credit card debt due to a hardship, it can feel like a desperate situation. You might be tempted to try and stretch the truth or even tell the creditor things that simply aren’t true in order to ensure that they’ll provide you with some relief.

You’ll want to resist this temptation. Instead, be honest about your situation and provide documentation that helps substantiate the claims you are making.

Depending on your situation, the types of documents you will want to submit are going to vary quite a bit. Here are some examples of documents you might consider including:

Are you trying to get on top of your credit cards and credit score? Check out these posts about hiding your credit utilization, getting an Amex card, department store cards for bad credit, and how getting a new credit card impacts your credit.

When you’ve gone through a difficult time, it can be difficult to separate essential from nonessential information in a hardship letter. It’s best to be concise and straightforward when writing while not getting too lost in the details of your situation.

If you are having a hard time determining which information should be included in your hardship letter, consider having someone you trust look over your draft before submitting it. Frequently, people that are outside of a situation are better able to identify the most important objective facts that you would want to share with your creditor in order to help them understand the hardship you have endured.

Templates and examples can be incredibly useful when you are learning how to write a hardship letter. However, if you simply insert your information into an online template, it won’t be specific to your circumstances and won’t come off nearly as genuine.

When writing this type of letter, you might be tempted to try and show the credit card company that you are worthy of assistance through your use of language. It can also feel awkward to write a letter to a creditor, and you might find yourself using bigger words than you normally would or relying on jargon to get your point across.

After you have written your draft, take a look and make sure that it reads smoothly and clearly. Typically, it’s best to stick with simple language. This can also help ensure that your letter is short and to the point.

When you’ve experienced hardship, it’s hard to not think about the factors, organizations, or people that contributed to your current situation. That being said, it’s best to not use your letter as an opportunity to cast blame on others. Instead, you’ll want to focus on explaining your situation in a clear and simple way.

Are you trying to boost your credit with a secured credit card? Take a look at this guide to learn how much of an increase you can expect when you take out a secured line of credit.

Your letter should emphasize the reason that you’re writing– to request hardship assistance. You will need to make a strong case that you are going through a difficult situation that makes it difficult if not impossible for you to remedy the situation without brokering a deal with them.

It’s important to go beyond simply explaining the trouble you’ve gone through. An essential section of your letter is where you express what it is that you want from the creditor.

What can the creditor do for you to help make it possible for you to pay off your debt without defaulting? You will have a much better chance of receiving the help that you need if you propose a clear action plan to your creditor.

Additionally, you’ll want to make it abundantly clear that the plan you are proposing is absolutely necessary in order for you to be able to continue paying off your debt.

As stated previously, it’s best to use examples and templates as inspiration for your own letter rather than simply inserting your information into an existing sample. That being said, it can be very useful to see examples in order to understand what a hardship letter should look like.

Your Name

Your Address

Your Phone Number

Name of Credit Card Issuer

Mailing Address of Credit Card Issuer

Credit Card Company Phone Number

RE: Hardship Letter

Date

To Whom It May Concern,

I am writing because I am experiencing financial hardship and would like to ask for a settlement of my credit card balance. My offer is to pay twenty-five percent of the outstanding balance on my account.

Over the last (X months), I have experienced a considerable decrease in my income. With the high-interest rate that is currently being charged on my account, I am unable to make the monthly payments in the amount of (X dollars.)

I have attached proof of my hardship in the form of the last three months of bank statements, my pay stubs, and copies of late payment statements. Please let me know if there is more information I can provide to help you understand my current financial hardship.

I am currently doing what I can to avoid filing for bankruptcy. In order to do so, I need to make debt settlement arrangements with creditors.

I ask that you please consider my settlement offer and accept it. At the point at which I receive your written agreement, I will send the payment within five business days.

Please don’t hesitate to contact me if you have any concerns or questions. You can contact me at (phone number) to discuss the settlement offer.

Thank you for your time.

Sincerely,

(Your name)

Your Name

Your Address

Your Phone Number

Name of Credit Card Issuer

Mailing Address of Credit Card Issuer

Credit Card Company Phone Number

RE: Hardship Letter

Date

Dear (name),

In this letter I will be explaining the unfortunate set of circumstances that have led me to fall behind on my credit card payments. I have done everything I possibly could to try and stay current with my bills, but the hardship I have experienced has made it impossible for me to do so. I am asking that you will work with me in my effort to pay off the debt that I owe by lowering my monthly payments to (X amount) temporarily for (X months).